Bitcoin exposure via ETFs has gone from novelty to mainstream, but not all funds will make the cut. In a market where liquidity begets more liquidity, scale is turning into a survival trait.

Recent flow data delivered a live stress test: heavy redemptions showed how investors gravitate to the deepest order books and the broadest authorized participant networks. Smaller funds, already juggling fixed costs and thinner spreads, are the ones that feel the squeeze first.

This piece examines why size matters for spot bitcoin ETFs, what the latest outflows reveal about competitive dynamics, and how to evaluate the closure risk that shadows sub‑scale products.

| Point | Details |

|---|---|

| Scale compounds liquidity | Larger ETFs attract tighter spreads, more market makers and steadier creations/redemptions, reducing trading frictions. |

| Outflows are a stress test | Industry‑wide redemptions shift flows into the most liquid tickers and can expose tracking slippage in smaller funds. |

| Fixed costs burden sub‑scale funds | Custody, compliance and market‑making support are relatively fixed, raising expense pressure when AUM is low. |

| Closure risk is real | Issuers sometimes withdraw new launches or wind down thin products; investors should monitor AUM, spreads and creation activity. |

| Investors can mitigate | Use a pre‑trade checklist: check spreads, daily volume, basket creation health, issuer stability and communications history. |

When ETF Scale Becomes a Survival Trait

Editor’s note: The late‑May redemptions were a clean reminder that liquidity concentrates in the biggest tickers when sentiment flips. Desk leads also flagged how AP participation narrows for smaller products during stress, which shows up immediately in spreads. Even new launches are getting more cautious—one issuer withdrew a crypto ETF registration in May. My own takeaway: sizing and execution plans matter as much as fees when you’re picking a bitcoin ETF for real money. — Elliot Veynor

Exchange-traded funds are network goods: tighter spreads attract more flow, which tightens spreads even further. For spot bitcoin ETFs, this flywheel is amplified by an additional layer—the authorized participant (AP) and market maker ecosystem that stands behind primary market creations and redemptions.

Large funds typically command the broadest AP rosters and deepest secondary market liquidity. That makes it easier for institutions to move size without moving the market, and it lowers the all-in cost of ownership (management fee plus trading frictions). Smaller funds can compete on niche exposures or differentiated operations, but the default advantage is with scale.

Pro tip: When screening ETFs, treat spread consistency across calm and volatile sessions as a core metric—not just the headline fee.

The Cost Math: Why Small Funds Struggle

Fixed and semi-fixed overheads

ETF businesses carry a base layer of costs that do not scale down well: regulatory filings, audit, listing fees, custody, insurance and critical relationships with APs and market makers. When AUM is small, these expenses represent a larger share of assets and pressure the fund’s economics.

Fee flexibility and price wars

Larger issuers often have room to set or maintain competitive fees because they can spread fixed costs over substantial AUM and cross-subsidize distribution. Smaller funds may need higher expense ratios or temporary waivers to break in—tactics that become harder to sustain through prolonged drawdowns or outflow streaks.

Distribution power

Placement on major platforms, model portfolios and advisory menus is not automatic. Scale and brand recognition help unlock those channels, feeding a virtuous cycle of visibility and flows that sub‑scale funds struggle to replicate.

Liquidity Effects: Spreads, Premiums and Trade Slippage

For any ETF, execution quality shows up first in the bid/ask spread and realized slippage. In spot bitcoin funds, liquidity also depends on how efficiently the AP network can source and deliver the underlying BTC, especially in fast markets.

- Spreads: Larger ETFs generally post narrower spreads because more market makers are quoting and hedging larger pools of inventory.

- Premium/discount control: With robust creations/redemptions, price gaps to net asset value (NAV) tend to be transient. Thin funds risk stickier deviations during stress.

- Trade capacity: Bigger secondary markets can absorb block trades with less footprint, reducing implementation shortfall for institutions.

Execution rule of thumb: If your order size is a notable share of a fund’s daily dollar volume, expect slippage—regardless of the underlying asset.

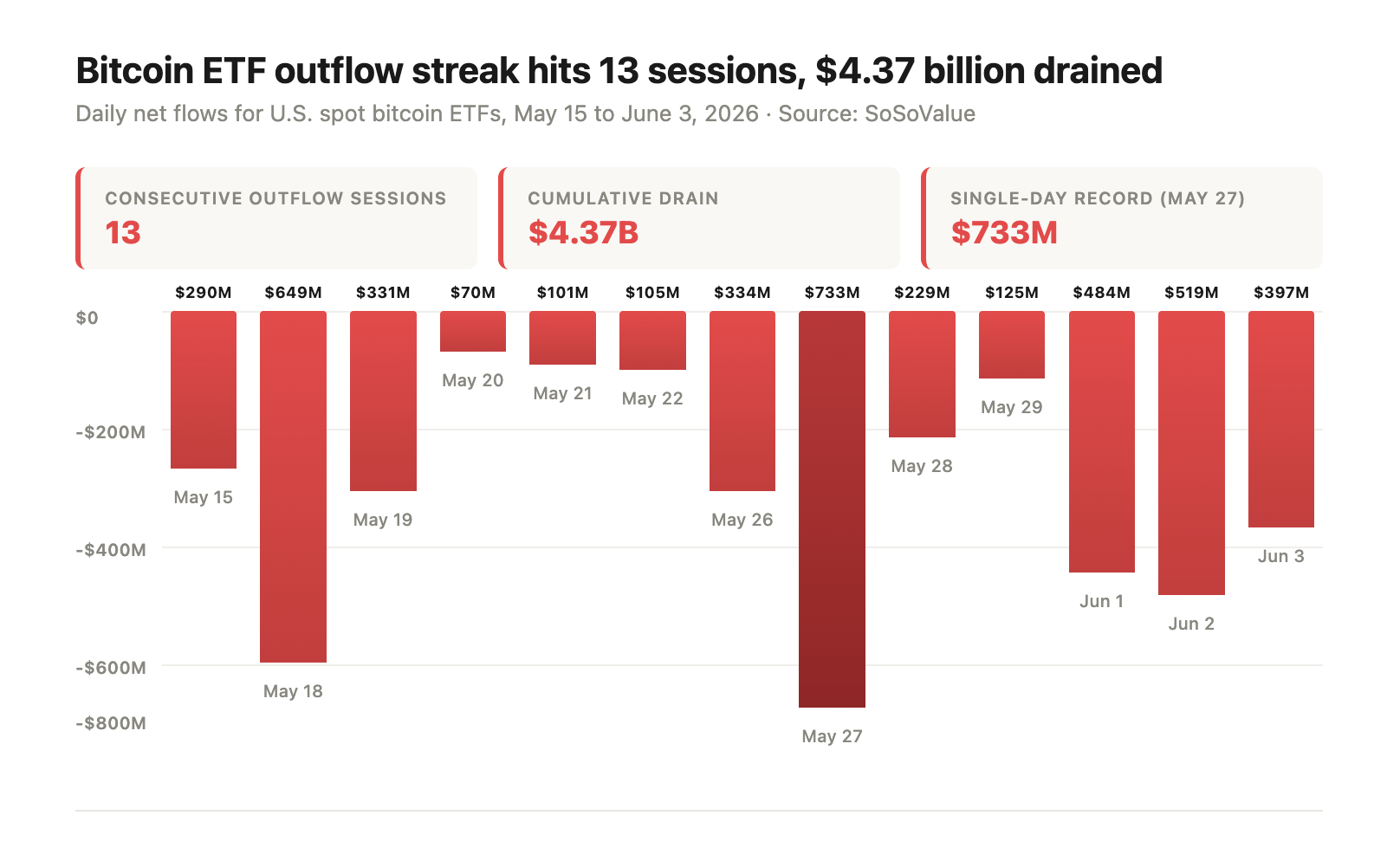

Stress-Test Lessons from May–June 2026 Flows

Recent data delivered a clear message about where investors run when the tide goes out. On May 28, 2026, BlackRock’s iShares Bitcoin Trust saw roughly $527.84 million of net outflows, while the cohort of 11 U.S. spot bitcoin ETFs shed about $733.43 million in a single day CoinDesk.

That was part of a broader nine‑day outflow streak totaling about $2.8 billion through May 29, 2026 CoinDesk. Across the same period, total assets in U.S. spot bitcoin ETFs fell from roughly $104.29 billion (May 15) to $82.83 billion by June 3–4—around a $21.46 billion decline in three weeks CoinDesk.

Three takeaways stand out:

- Liquidity flight: When sentiment turns, redemptions concentrate in the most trafficked tickers, because those funds offer the cleanest exits.

- Operational resilience matters: The ability to keep creations/redemptions smooth under heavy flows is a differentiator—small funds dependent on a narrow AP roster face more friction.

- Distribution reach buffers pain: Products embedded in institutional workflows (models, SMAs, pensions) can experience steadier activity than those relying on episodic retail flows.

At the same time, the funnel of new launches is showing signs of caution. In May 2026, Yorkville America Digital—known for its association with Truth Social—formally asked the SEC to withdraw its registration statement for the Truth Social Crypto Blue Chip ETF, citing a decision not to pursue the offering at this time SEC EDGAR (Yorkville withdrawal letter). Pullbacks like this illustrate how the bar to enter (and remain) in the market is rising.

Identifying Closure Risk: A Practical Checklist

ETF closures are a normal industry cleanup, but investors can avoid unnecessary friction by watching for the warning signs. Use this checklist before allocating and during periodic reviews:

- AUM trajectory: Absolute size matters, but the direction matters more. Stagnant or shrinking AUM over multiple quarters can signal pressure.

- Average daily volume and spreads: Look for consistent liquidity during both calm and volatile days. Wide, unstable spreads are a red flag.

- Creation/redemption health: Persistent creation halts or unusually small primary market activity can indicate operational strain.

- Issuer breadth and product shelf: Multi‑product, multi‑billion issuers usually have more staying power than single‑fund shops.

- Fee waivers and temporary discounts: Useful for launch, but if extended repeatedly, they may hint at difficulty achieving scale.

- Communications history: Transparent, timely updates from the issuer—especially during stress—are positive signals.

- Market maker depth: Multiple active liquidity providers reduce the risk of spread blowouts.

Pro tip: Cross‑check multiple data sources (issuer website, exchange data, and reputable market trackers) to confirm AUM and volume. Data lags are common around rebalances and holidays.

How Fund Shutdowns Work in Practice (and How to Prepare)

What typically happens

When an ETF winds down, the issuer usually announces a last trading day and a liquidation date. Trading may continue for a window, with creations halted to enable an orderly unwind. After liquidation, investors receive cash at the fund’s NAV less costs as disclosed in the prospectus. Timelines and specific mechanics vary by issuer and exchange rules.

Investor impacts

- Forced turnover: Your exposure converts to cash, which may introduce timing risk versus your target allocation.

- Tax considerations: Liquidation can be a taxable event; treatment depends on jurisdiction and cost basis.

- Trading frictions: Spreads can widen into the last trading days. Liquidity usually thins as APs and market makers scale down activity.

Preparation steps

- Document your preferred alternatives ahead of time (e.g., two replacement tickers with adequate liquidity).

- Set alerts for issuer press releases and exchange notices concerning creations, redemptions and last trading dates.

- Plan exit windows to avoid end‑of‑life spread spikes; use limit orders to control execution.

- Coordinate with tax and compliance teams if managing client assets to pre‑empt reporting surprises.

Choosing Between Giants and Niche Players

Scale is a powerful moat, but it is not the only lens. Some investors prefer niche exposures—like region‑specific custody, ESG overlays, or operational features that align with mandates. The question is whether the differentiation is durable enough to offset the liquidity head‑start of the leaders.

When the giant makes sense

- You prioritize tight spreads and block trade capacity.

- You need predictable creations/redemptions across market regimes.

- You want the broadest distribution support and operational redundancy.

When a niche fund can justify the choice

- The fund delivers a feature you cannot replicate elsewhere, and your sizing is modest relative to its daily dollar volume.

- You have a multi‑ETF policy (primary plus backup) and accept potential turnover if the niche fund does not scale.

- The issuer demonstrates clear transparency on basket operations, counterparties and risk controls.

Daily net-flow chart for U.S. spot Bitcoin ETFs (May 15–June 3, 2026) showing a 13‑session outflow streak totaling ~$4.37B — visual evidence of how rapid redemptions can shrink AUM and stress smaller or higher‑cost funds. — Source: CoinDesk

Mistakes to Avoid in Bitcoin ETF Selection

- Chasing the lowest fee in isolation: A few basis points saved can be overwhelmed by wide spreads or poor execution.

- Ignoring creation activity: A healthy primary market is the backbone of fair pricing; watch for pauses and unusual deviations from NAV.

- Overlooking issuer stability: A diversified product shelf and sustained communications record reduce operational risk.

- Buying size relative to volume: Oversized orders in thin funds invite slippage; consider slicing or using a more liquid vehicle.

- Assuming all bitcoin exposure is identical: Custody setups, insurance, and operational partners vary and affect risk.

What the Recent Withdrawals Signal About Competition

The decision by Yorkville America Digital to withdraw its registration for the Truth Social Crypto Blue Chip ETF in May 2026 underscores a tougher competitive landscape for newcomers SEC EDGAR (Yorkville withdrawal letter). Launching into a market now dominated by a handful of scaled tickers means heavier marketing spend, sharper fee pressure and a higher bar to win AP and market‑maker commitment.

Combine that with the late‑May flow shock—IBIT’s large single‑day outflow and the nine‑day, multi‑billion streak across the category CoinDesk, CoinDesk—and it becomes clear why some prospective issuers prefer to sit it out. For investors, the signal is straightforward: favor funds that can operate through both inflow surges and redemption waves without disrupting price formation.

A Quick Heuristic for Evaluating Scale

There is no universal cutoff that guarantees longevity, but practitioners often lean on multiples rather than hard numbers. Consider:

- Liquidity multiple: Is the fund’s average daily dollar volume at least several times larger than your typical order size?

- Spread stability: Do spreads remain narrow during volatile bitcoin sessions?

- AP diversity: Does the issuer disclose a broad AP/market‑maker roster or demonstrate resilience during prior stress events?

- AUM relative to peers: Is the fund meaningfully scaled versus the top quartile, or locked in the long tail?

- Resilience track record: How did the fund behave during the late‑May 2026 outflows and the subsequent AUM drawdown to early June CoinDesk?

For more market‑tested context, Crypto Daily regularly tracks ETF flows, spreads and issuer moves to help readers benchmark their choices without the hype. You can find coverage and data roundups at Crypto Daily.

Frequently Asked Questions

Do bitcoin ETFs ever close, and what triggers it?

Yes. Closures can follow sustained sub‑scale AUM, high relative costs, or strategic refocusing by the issuer. Periods of heavy outflows and fee competition increase pressure on thin products. In some cases, proposed launches are withdrawn before listing when market conditions or economics look unfavorable, as seen with Yorkville America Digital’s May 2026 withdrawal filing.

How would a closure affect my position?

The issuer typically announces a final trading date and a liquidation date. Trading may continue for a period with creations halted. After liquidation, you receive cash at NAV (less costs). Expect thinner liquidity and wider spreads near the end; using limit orders and pre‑planning a replacement ticker can help.

Is fee level or liquidity more important?

Both matter, but for practical implementation costs, liquidity (spreads, depth, creation health) often dominates. A small fee advantage can be overwhelmed by slippage if a fund trades thin or deviates from NAV during stress.

What’s a reasonable AUM level for comfort?

There is no universal threshold. Many practitioners focus on momentum and peer rank rather than a single number—prefer funds with rising AUM, robust daily volume, and a visible AP network over those stuck in the long tail.

Do large single‑day outflows mean an ETF is broken?

Not necessarily. Outflows reflect investor positioning. The key test is whether creations/redemptions function smoothly, spreads stay orderly, and pricing aligns closely with NAV during heavy flow days. In late May 2026, outflows were broad across the category, not isolated to one issuer.

How can I check creation/redemption activity?

Look for issuer notices, exchange data and trusted market trackers that report primary market activity and basket information. Persistent creation halts or unusual NAV deviations are caution flags.

Are niche bitcoin ETFs doomed to close?

Not by default. If a niche adds real value and manages costs, it can survive. However, in sustained risk‑off regimes and fee wars, sub‑scale funds face higher hurdles. Diversifying across primary and backup tickers can reduce operational concentration risk.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Be the first to comment