CoinShares set a 12-month base-case target of $3.50 on Gram (GRAM), previously known as Toncoin, in a report by research head James Butterfill, built when the token traded at $2.40. Gram now changes hands near $1.60, having surrendered the entire rally triggered by Telegram’s takeover of the network.

The report’s thesis, that Telegram gives GRAM the best user funnel in crypto but the token still has to prove people will actually use it, is being stress-tested in live markets faster than the report anticipated.

Key Takeaways

- CoinShares base case of $3.50 implies roughly 119% upside from the current $1.60.

- Telegram has ~1 billion monthly users; TON has 1.78 million monthly active wallets.

- Roughly 37 million GRAM unlocks every month through late 2028.

- Price is pinned between the 200-day average at $1.56 and the 100-day at $1.66.

The Best Funnel in Crypto, Barely Used

The market consensus treats Telegram’s involvement as Gram’s superpower. The report agrees on distribution and then delivers the caveat that matters. In June Butterfill wrote that “TON has solved distribution better than any Layer 1 to date.” The rest of the report explains why that has not been enough.

The numbers behind the caveat are stark. Telegram counts around 1 billion monthly users and roughly 500 million daily ones. More than 100 million of them have touched digital assets through the integrated TON Wallet. Yet only about 1.78 million wallets are active on the chain in a given month, roughly 0.12% of Telegram’s user base. Daily transactions run near 2.16 million, against roughly 72 million on Solana. Total value locked on the network sits around $69 million at the time of writing, down from a July 2024 peak near $740 million.

In plain terms: Telegram built a stadium for a billion people, and about one in every 800 of them has walked in. The investment case is a bet that the doors just opened, not that the crowd is never coming.

The strongest counter-evidence is stablecoins. USDT liquidity on TON has grown past $750 million, and the report identifies Telegram-based cross-border payments as the most credible non-speculative demand driver. On that use case, TON looks less like a smart-contract chain competing with Ethereum and more like a payments rail bolted into a messaging app.

What Telegram Actually Changed This Spring

The takeover was the third step of Pavel Durov’s “Make TON Great Again” campaign, a seven-step roadmap that has driven every major Gram move this year. Catchain 2.0 activated on April 9, cutting block production from about 2.5 seconds to 400 milliseconds and finality from roughly 10 seconds to about 1 second. On May 1, base transaction fees were cut roughly sixfold to about $0.0005, cheap enough for the micro-payments Telegram’s mini-apps need. On May 4, Telegram formally replaced the TON Foundation as the network’s operator and became its largest validator, staking about 2.2 million GRAM.

The market’s answer was violent. Gram rose roughly 79% in the seven days to May 11, spiking from about $1.35 to a wick near $2.90 on the heaviest volume of the year, visible as the vertical candle cluster on the daily chart. The rebrand followed: on June 1 Durov announced Toncoin would reclaim its original 2018 name, a community vote passed with 81.22% support, and the change took effect June 15 with no token swap required, The Block reported. Three steps of the roadmap remain undisclosed.

Then the premium bled out. Over May and June the token gave back the entire takeover rally in a two-month decline, and the pattern is now familiar: each roadmap step produces a spike, and each spike fades once the announcement is absorbed. Markets are paying for news, not yet for usage.

What the Chart Says at $1.60

TradingView’s daily chart shows Gram compressed into a narrow decision zone. Price at $1.60 sits just above the 200-day simple moving average at $1.558, the long-term trend line that acted as the floor through most of June, and just below the 100-day at $1.663. The 50-day average at $1.712, still sloping downward from the May peak, caps the structure above.

The early-July attempt to break that stack tells the near-term story. Gram climbed from the $1.55 area in late June to almost $1.80 by July 7, clearing both the 100-day and 50-day averages intraday. The move failed in a single session: a heavy red candle on July 7 erased four days of gains and dropped price straight back below the 100-day. That is the second lower high since the May peak, and it leaves $1.75 to $1.80 as confirmed supply.

The levels from here are clean. Holding the 200-day at $1.56 keeps the recovery structure alive; a daily close below it opens the June floor near $1.50, and below that the pre-takeover range around $1.30 to $1.35, which is where the entire Durov premium would be fully unwound. On the upside, a close above the 100-day at $1.66 is the first requirement, a break through $1.80 the second. The CoinShares $3.50 base case sits far above anything the current chart structure supports, which is precisely why the report frames Gram as a selective satellite position rather than a core holding.

What the Order Flow Adds to the Picture

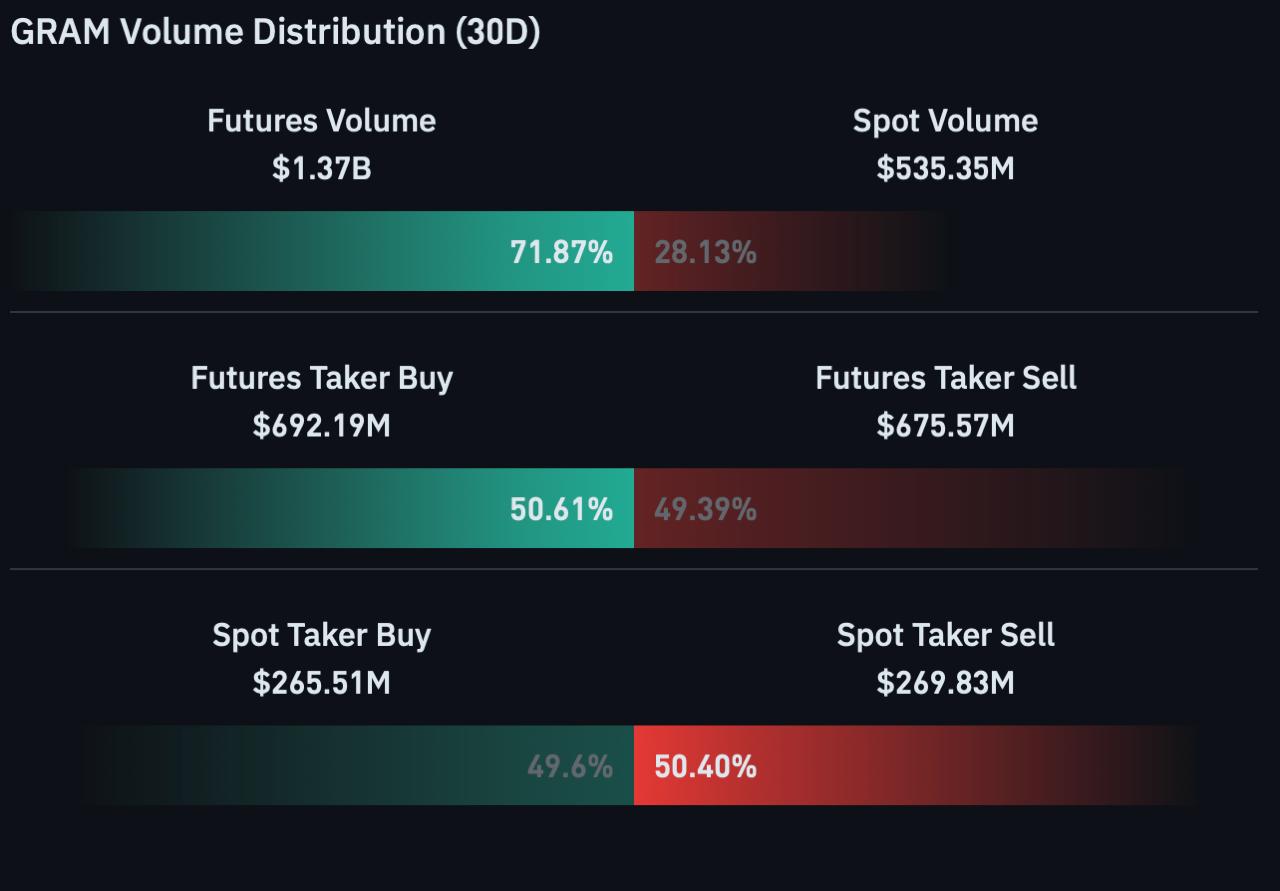

Derivatives data sharpens the read. Futures account for $1.37 billion of Gram’s 30-day trading volume against $535 million in spot, a 72-to-28 split, according to CoinGlass data. Gram remains a leverage-driven market, which helps explain why roadmap announcements produce such sharp spikes and equally sharp reversals: fast money arrives first and leaves first.

What the flow does not show is conviction in either direction. Over the past 30 days, aggressive futures buying and selling are nearly dead even at 50.6% versus 49.4%, and spot flows mirror it at 49.6% buy versus 50.4% sell. Taker flow measures the side willing to pay the market price to get filled immediately, so a near-perfect balance means neither bulls nor bears are pressing. That is the order-flow signature of the same compression visible on the price chart.

The one divergence worth watching sits in the most recent session. Futures activity has cooled sharply, with 24-hour volume running at just 39% of its weekly average and sellers holding a slim 51% edge, while spot volume is running 38% above its 30-day average with buyers dominant at 52.5%. Leverage is stepping back while spot demand quietly firms. It is a small sample, one day of data, but it is the healthier pattern: ranges built by spot accumulation tend to resolve more durably than ranges propped up by leveraged positioning.

The Supply Problem the Price Drop Made Worse

The report’s biggest flagged risk is the unlock calendar, and the decline since publication has sharpened it in one way and softened it in another. About 1.08 billion GRAM, roughly 21% of total supply, is being released through monthly unlocks of about 37 million tokens into late 2028. At the report’s $2.40 price, that meant roughly $90 million of potential monthly sell pressure against an estimated $30 million to $50 million of observable monthly demand. At $1.60, the same unlocks translate to about $59 million per month, closer to the demand band but still above its midpoint. Less dollar pressure, same token flood, and a market that now has less confidence to absorb it.

The yield story cuts the other way. After Catchain 2.0, gross staking yield jumped from 0.34% in March to an annualized rate near 16.7% according to Butterfill, with net institutional yield estimated at 14% to 16%, above Ethereum and Solana on nominal terms. The report is careful to call this partly illusory, since unlock dilution eats into the real economic return through 2028. High headline yield built partly on new token issuance is a familiar crypto pattern, and it rewards reading the fine print.

Two structural risks sit under everything. Gram is not Telegram equity, and the report is explicit that holders have no claim on Telegram’s revenue or any future IPO; the token is infrastructure exposure to Telegram’s payments economy, nothing more. And the dependency runs one way: TON now leans on a single company, a single founder facing an ongoing French criminal case, and a validator set in which that company is the largest player. Telegram’s history with regulators is not hypothetical. The SEC forced it to abandon this same network in 2020, returning $1.22 billion to investors, and the revived Gram name is a bet that the climate which allowed that outcome is gone for good.

The technical reality suggests Gram’s next move depends less on the remaining roadmap steps than on whether conversion data starts moving: active wallets, stablecoin settlement, mini-app fees. The funnel is built, the chain is now fast and cheap enough to use, and the early order-flow shift toward spot is the first faint signal worth tracking. What the price at $1.60 says is that the market has stopped paying for the promise and started waiting for the proof.

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency markets are volatile and involve substantial risk. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.

Be the first to comment