Author

Ahmed Barakat

Author

Share

Fact Checked by

CryptoNews Editorial Team

Author

SWIFT is taking its biggest step into crypto after confirming its blockchain-based shared ledger is ready for initial use. Built on Hyperledger Besu over nine months, the network will let 17 major banks, including HSBC, Citi, UBS, BNP Paribas, DBS, ANZ, and Standard Chartered, pilot live cross-border payments using tokenized deposits.

The rollout moves beyond closed sandbox testing into real banking operations. Rather than replacing existing payment rails, the ledger coordinates tokenized deposits between participating banks while final settlement stays on the current infrastructure. That could help banks process payments during nights, weekends, and across time zones, where delays have long been a problem.

Discover: The Best Token Presales

What the SWIFT Crypto Ledger Actually Does

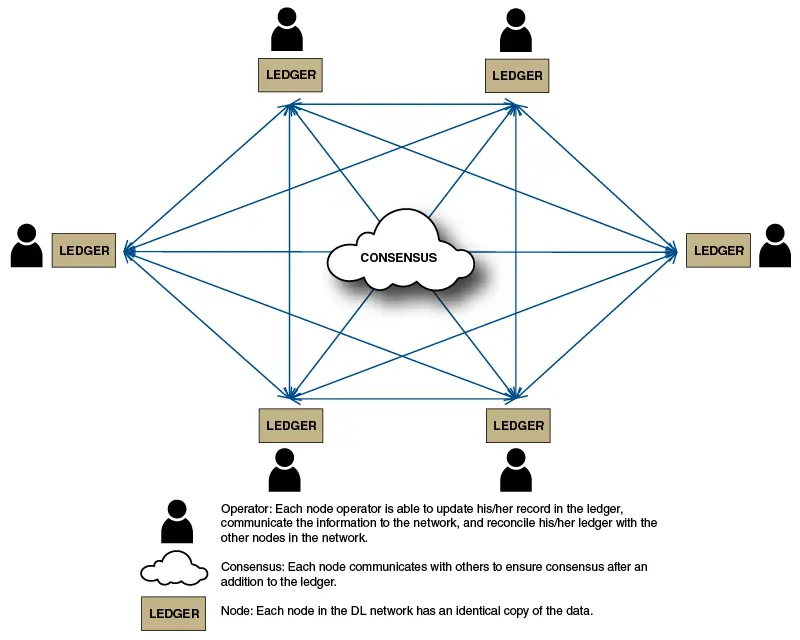

The shared ledger sits above existing payment rails instead of replacing them. When a participating bank starts a transaction, the platform coordinates funding commitments across counterparties and gives every institution the same real-time view of payment status. Final settlement still runs through RTGS systems and Swift’s existing messaging network.

The pilot uses bank-issued tokenized deposits rather than stablecoins or public crypto assets. Each token is backed one-to-one by commercial bank deposits, giving it the same regulated status as money held in a traditional bank account. In practice, the blockchain improves how banks move and coordinate funds, while the underlying money and compliance framework remain unchanged.

SWIFT already processes 75% of payments to beneficiary banks within 10 minutes on existing rails, often in seconds. The ledger’s specific contribution is removing the remaining constraint: the dependency on overlapping business hours between sender and receiver.

The result is 24/7 settlement availability, including overnight and weekend flows that current infrastructure cannot support, regardless of how fast the underlying messaging moves.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Compliance Architecture Is the Strategic Signal

One reason the crypto project could gain traction is what Swift chose not to change. The shared ledger keeps the compliance, credit, risk, and control standards already used in today’s payment systems. Instead of creating a separate settlement network, it works within the existing regulatory framework.

That approach matters because regulators and major banks have been reluctant to adopt tokenized payment systems that weaken oversight. By keeping established safeguards in place, Swift is pitching blockchain as an upgrade to existing infrastructure rather than a replacement for it.

Thierry Chilosi, Swift’s Chief Business Officer, said the platform lets tokenized value move across borders with the speed modern commerce demands while maintaining the resilience, security, and compliance expected by global financial institutions.![]()

The pilot brings together 17 banks from six continents, including ANZ, BNP Paribas, BNY Mellon, Citi, DBS, First Abu Dhabi Bank, FirstRand Bank, HSBC, Itaú Unibanco, Lloyds Bank, Mashreq, MUFG Bank, OCBC, Standard Chartered, UBS, UOB, and Wells Fargo.

The lineup suggests this is more than a regional trial. These institutions play a central role in cross-border payments across the dollar, euro, and major Asian currency corridors. Their participation gives the project a broader international footprint from the outset and could provide an early test of blockchain-based settlement at global banking scale.

Discover: The Best Crypto to Diversify Your Portfolio

The Broader Institutional Tokenization Race

SWIFT is not operating in isolation. A separate consortium including JPMorgan Chase, Bank of America, Barclays, and BNY Mellon announced a US-focused tokenized deposit network via The Clearing House, targeting a first-half 2027 launch.

NYSE parent Intercontinental Exchange has outlined a 24/7 settlement venue for tokenized securities with stablecoin-based funding, while NYSE itself partnered with Securitize in March to build blockchain infrastructure for tokenized stocks and ETFs.

Payments, deposits, and securities are steadily moving toward a blockchain-based infrastructure that can operate around the clock. Swift’s pilot stands out because of its reach. Its existing network connects more than 11,500 financial institutions across over 200 countries, giving the shared ledger a potential user base that few blockchain payment networks can match.

If the pilot succeeds across 17 major banks and multiple currency corridors, it could make it easier for other institutions to join. The project is designed to work within existing banking rules, reducing one of the biggest barriers to institutional adoption.

Swift has already outlined the next phase. Future upgrades are expected to support foreign exchange payment versus payment, programmable corporate payments, and cash movements tied to securities transactions. The current rollout is an early milestone, while the next test is whether that global network can translate interest into meaningful transaction volume.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Be the first to comment