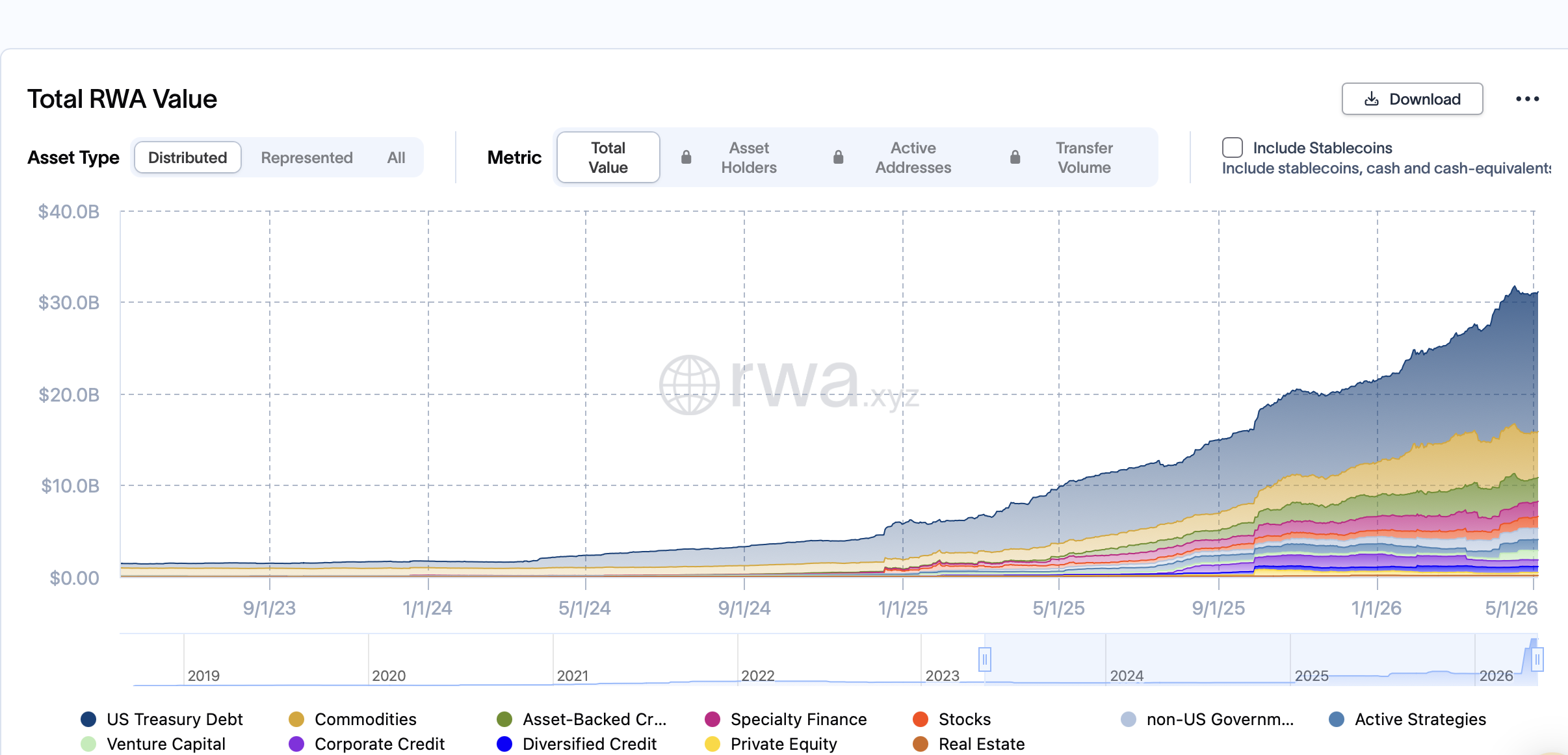

The tokenized real-world asset market has crossed $31 billion on the latest RWA.xyz total-value view, with total RWA value at about $31.12 billion. The dashboard also separates other measures, including distributed asset value, represented asset value, asset holders, and stablecoin value, which is why the exact headline number depends on the selected RWA.xyz view.

Stablecoins remain a separate base layer on RWA.xyz, with total stablecoin value near $299.30 billion and more than 241 million holders. The non-stablecoin RWA market now spans Treasuries, credit, commodities, equities, funds, active strategies, and real estate, while stablecoins still provide the cash leg for payments, redemptions, collateral movement, and settlement.

RWA.xyz tracks U.S. Treasuries, non-U.S. government debt, credit products, commodities, stocks, private equity and venture capital, active strategies, and real estate. A recent RWA.xyz review covered how that breadth makes the platform useful for issuers, analysts, protocols, and institutional users following tokenized assets.

Treasuries, Credit And Gold Lead The Stack

RWA.xyz’s largest listed products show how broad the market has become. Figure’s HELOC token represented more than $16.25 billion in asset-backed credit value. Circle’s USYC was near $2.61 billion, BlackRock’s BUIDL stood around $2.14 billion, Ondo’s USDY was near $1.51 billion, Janus Henderson Anemoy’s JTRSY was above $1.04 billion, and Franklin Templeton’s BENJI was near $1.02 billion.

Commodity-backed products also remain significant. Tether Gold’s XAUT was around $2.53 billion, while Paxos Gold’s PAXG was near $2.27 billion. Tokenized credit products showed about $5.62 billion in distributed value on RWA.xyz’s credit dashboard, with represented credit value above $21 billion.

Network concentration remains clear. Ethereum led the RWA network table with about $15.5 billion in total value and a 58% market share. BNB Chain followed with about $3.4 billion, while Solana held around $1.7 billion. Stellar, Liquid Network, Arbitrum, Avalanche, XRP Ledger, Plume, and Polygon rounded out the top network group.

The market has also started moving into equity-like products. A recent Securitize, Jump, and Jupiter launch on Solana showed how tokenization is expanding from Treasuries into stocks, ETFs, private credit, and institutional funds.

BounceBit’s Productive Collateral Thesis Fits The Data

The RWA growth path reinforces BounceBit’s core argument that tokenized assets should not sit idle after issuance. BounceBit’s RWA yield documentation describes a dual-yield model where RWA tokens can continue earning base yield from traditional financial instruments while also serving as collateral for delta-neutral trading strategies.

That model treats tokenized Treasuries and money-market products as usable balance-sheet assets rather than simple blockchain wrappers. A tokenized Treasury fund can generate underlying yield, support a credit line, back trading exposure, or become collateral in a structured strategy without being sold first. The same logic is starting to define the wider RWA conversation: tokenization creates the asset representation, but utility comes from custody terms, redemption design, collateral eligibility, trading access, and risk controls.

This is where the RWA market becomes more demanding. Tokenized Treasuries are not the same as tokenized private credit, and both differ from gold tokens, equities, or real estate. A recent private-credit comparison explained why yield, liquidity, credit risk, and redemption terms must be separated by asset class. Another RWA risk guide covered the custody, redemption, liquidity, and regulation risks that decide whether tokenized products can function safely inside DeFi.

The current RWA.xyz data supports the stronger market claim: total tokenized RWA value has moved above $31 billion, represented assets are far larger, and stablecoins remain a separate $299 billion base layer. The sector is broadening into credit, funds, commodities, equities, Treasuries, and active strategies, and the strongest products will be judged by what they can do after issuance: settle faster, redeem reliably, serve as collateral, connect to credit, and move through trading infrastructure without hiding the risks attached to the underlying asset.

Be the first to comment