The views expressed in this article are those of the author and do not necessarily reflect the position of CoinGeek.

I have been watching infrastructure manias play out for my entire adult life, and they all end the same way. If somebody borrows too much money to build something the market isn’t ready to pay for at scale, the music stops, and the bondholders get a haircut. The names change, and someone else benefits from the investment.

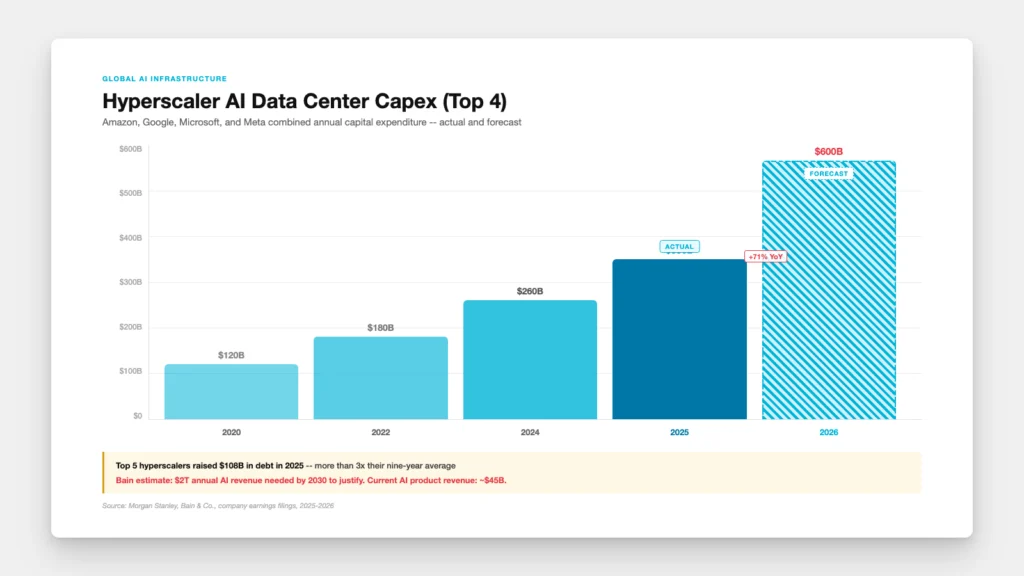

The current mania is artificial intelligence (AI) data centers. Amazon (NASDAQ: AMZN), Google (NASDAQ: GOOGL), Microsoft (NASDAQ: MSFT), and Meta (NASDAQ: META) are on pace to spend $350 billion in capex alone in 2025. The top five hyperscalers raised $108 billion in debt last year, more than three times their average over the past 9 years. By 2026, the analyst forecasts annual spending of $600 billion.

Bain & Company says the industry needs $2 trillion in annual AI revenue by 2030 to justify the math. Current AI product revenue sits at roughly $45 billion, a hair under what Apple’s iPad (NASDAQ: AAPL) division did last quarter.

That gap is bigger than the GDP of most countries on the planet. We have seen this movie before.

The interesting question is what we are left with when the credits roll, because this time the answer is genuinely different from every other infrastructure bust I have studied.

The railroad companies died. The iron did not.

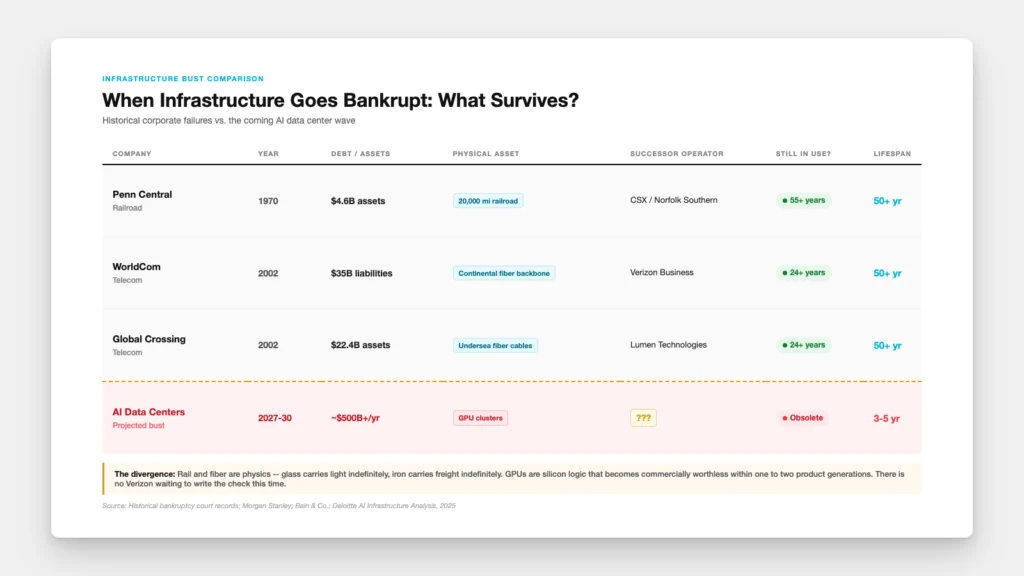

Every infrastructure boom in American history has ended in a wave of bankruptcies, and each of those bankruptcies has left behind something useful for the next operator.

Penn Central Transportation filed for bankruptcy in June 1970, with $4.6 billion in assets and an empire of more than 20,000 miles of track running from Boston and Montreal to St. Louis and Chicago. Roughly one-eighth of the entire U.S. freight network was inside the case. The company was so over-leveraged and so badly mismanaged that Congress had to create a federal rail corporation, Conrail, just to keep freight moving while the lawyers picked over the bones.

Now look at what happened to the iron. Conrail eventually broke up. CSX took the southern half. Norfolk Southern took the northern half. Both are Class I freight railroads today, and the same rails Penn Central laid are still moving trains in 2026. The bankruptcy killed a company. The infrastructure outlived it by more than half a century.

The telecom bust was similar in scope, but with a new kind of “rail” for data instead of trains. WorldCom filed in July 2002 with $35 billion in liabilities, the biggest U.S. bankruptcy of its era. The continental fiber-optic backbone they had built emerged from court as MCI, then got swallowed by Verizon for $7.6 billion in 2006. It is still carrying enterprise traffic for Verizon Business today. Global Crossing filed that same year with $22.4 billion in assets and $12.4 billion in debt. Singapore Technologies Telemedia and Hutchison Whampoa picked up the undersea cables for $750 million. Those strands eventually got absorbed into Level 3, then Lumen, and they still light up half the planet’s transoceanic data traffic.

In 2002, only 2.7% of the fiber laid during the boom was actually carrying a signal. By 2004, somewhere between 85 and 95% of all installed fiber was still dark. It took nearly a decade for demand to catch up. When it did, that dark fiber became the physical substrate for residential broadband and every video stream you have watched in the twenty years since.

Generational infrastructure, salvaged from generational bankruptcy, and that is the pattern the AI capex sales pitch is borrowing from. The argument goes that even if the current investors get crushed, the buildings will still be there, the racks will still be racked, and the next operator will turn it all into the cloud computing backbone of the next 50 years.

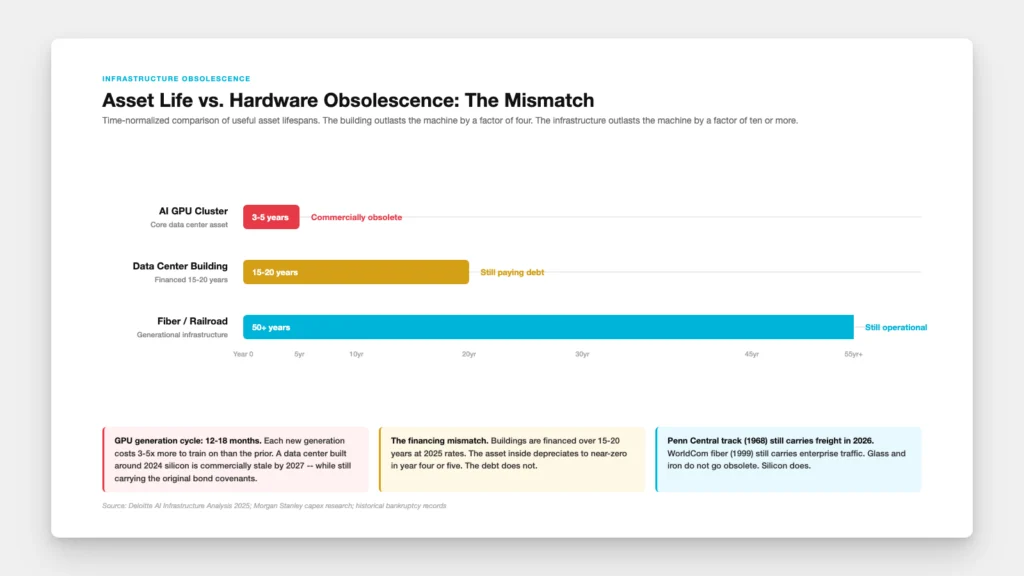

GPUs are not fiber

A strand of glass laid in 1999 carries a signal in 2026 just fine. It needs lasers on each end and a customer at the other side. The glass itself does not go obsolete. A railroad track laid in 1968 carries a freight train in 2026 if you maintain the ties and the ballast.

GPUs go obsolete. Fast.

The useful life of an AI processor sits somewhere between three and five years, but Nvidia (NASDAQ: NVDA) is shipping a new flagship every twelve to eighteen months, and each generation costs three to five times more to train on.

Deloitte’s own infrastructure analysis flags new AI chips launching “every few months” as an explicit risk for anyone building a multi-billion-dollar facility around current silicon. The building can be financed over twenty years. The silicon inside it is functionally stale before the carpet in the offices is even broken in.

When this wave breaks, the bankrupt operators will be selling depreciating door-stoppers. A two-cycle-old H100 cluster is not a Penn Central freight corridor. It is a warehouse full of expensive paperweights with electricity bills. There is no Verizon waiting in the wings to write a check, because the asset on offer is already obsolete on the day the gavel falls.

So, in this industry, we are sitting on a divergence nobody on Wall Street wants to underwrite.

Anyone who has spent a few minutes inside Bitcoin, or more specifically in the mining sector, can recognize the dynamic, because we live through our own version of it. The next flagship Antminer might be outcompeted by the next-next flagship miner before the generation installed last quarter even needs its first dust blow-out service.

But it is not all doom and gloom

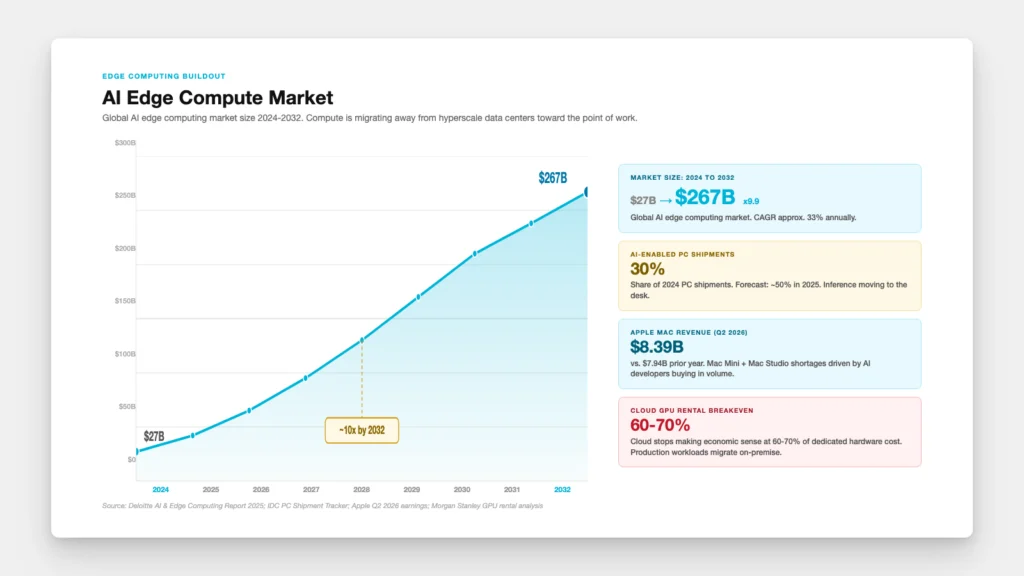

The bust is real and almost certainly unavoidable. The underlying technology trend is going nowhere because people aren’t going to just quit using AI tools. The compute is just going to move to places the hyperscaler bond underwriters did not include in their spreadsheets.

Look at where the actual demand is showing up. Apple posted $8.39 billion in Mac revenue last quarter, and Tim Cook openly said the Mac Mini and Mac Studio shortages were driven by AI developers buying them in volume to run agent platforms at the edge. A $400 consumer desktop has quietly become an enterprise tool, because the actual work people want to do with AI (inference, agent orchestration, fine-tuning small models, vibe coding entire applications) does not require a hyperscale data center. It requires a competent piece of silicon and a fast bus.

Deloitte put a number on the same trend. The global AI edge computing market was $27 billion in 2024 and is projected to hit $267 billion by 2032. Cloud GPU rentals stop making economic sense at 60 to 70 percent of dedicated hardware cost, and once you are running production AI workloads at any meaningful scale, the on-premise math wins.

In short, the hyperscalers are spending half a trillion dollars to host workloads that are migrating away from them in real time.

There is a second dynamic compounding the first. Models keep getting more efficient. The capability you needed a rack of GPUs to deliver in 2023 runs on a laptop in 2026.

In all likelihood, the next iteration runs on a phone. The compute requirements at the point of work are collapsing exponentially, even as the compute requirements at the frontier of training keep climbing.

So if the compute is escaping the hyperscaler, where is it actually going?

As I said above, it’s going to the edge, into Mac Minis and AI-enabled PCs sitting under desks.

It’s also going up. All the way up…

The optimistic scenario is in orbit

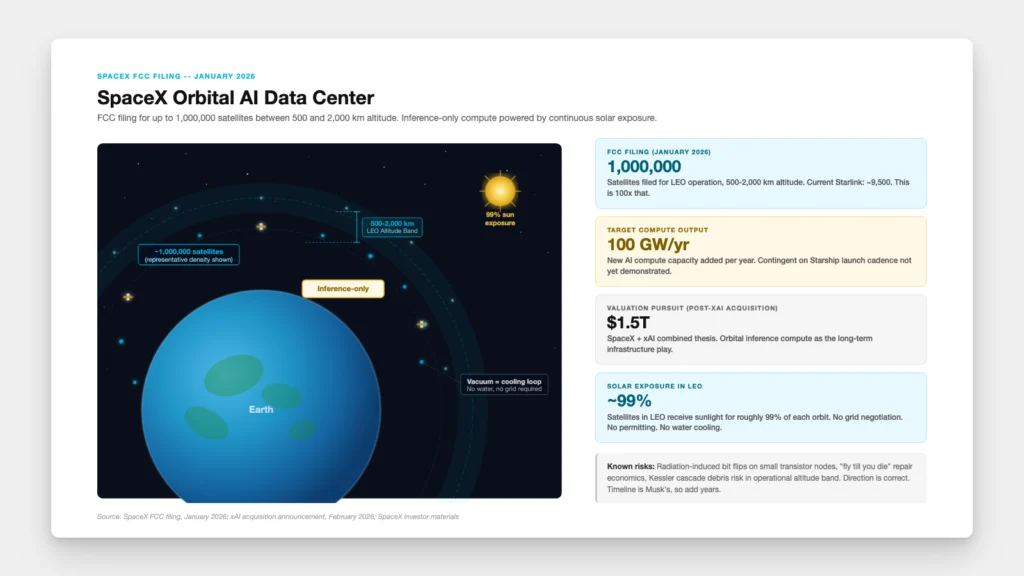

In January, SpaceX filed with the FCC for permission to operate up to one million satellites between 500 and 2,000 kilometers above the planet. The current Starlink constellation is around 9,500 birds. The proposal is for a hundred times more. The pitch is straightforward and clean. Solar panels in low Earth orbit see the sun for roughly 99% of every orbit. There is no electric grid to negotiate with. The vacuum of space is the cooling loop, the sun is the power plant, and the orbital slots are essentially free until the FCC and the ITU start fighting over who gets to assign them.

Elon Musk‘s stated target is 100 gigawatts of new AI compute capacity added every year, contingent on Starship hitting a launch cadence that does not currently exist anywhere on Earth.

SpaceX acquired xAI in February and is reportedly seeking a $1.5 trillion valuation, built largely on this thesis. The whole stack is positioned as inference compute rather than training compute, which is honest, because the failure modes (radiation-induced bit flips on small transistor nodes, “fly till you die” repair economics, debris cascade risk in the operational altitude band, and unsolved orbital training coordination at scale) are still genuinely open questions for the hottest workloads.

It is going to take longer than Musk says, just like most things he says. In fact, where’s my personal robot assistant, by Hyperloop access or my Miami Boring Tunnel?

Anyway, it’s easy to criticize Musk, but it’s also dangerous, because he aims high, fails high, and lands high, even if it wasn’t exactly where and when he said it would happen, but he’s rarely been totally “wrong” about the future.

And when it comes to orbiting data centers, I think the direction is right because sunlight and vacuum are infrastructure that nobody depreciates.

What actually happens from here

The data center bankruptcies are going to be ugly because the assets cannot be salvaged the way railroad tracks and fiber cables were salvaged. The companies that are 90% leveraged into GPUs that will be two generations old by the time the next debt covenant gets tested are not going to find buyers waiting in the wings. The smart money is already pricing this in, which is why the hyperscalers are racing to monetize before the music stops.

Underneath the bust, the actual compute revolution keeps moving. It goes down to the edge, where a Mac Mini under your desk is doing work that needed a rack in 2024. It goes up into a low Earth orbit constellation that uses sunlight for its thinking and the vacuum of space to dump its heat.

The losers in this cycle are the people borrowing 2026 dollars to buy 2027 silicon to run inside a 2045 building. The winners are the people who already understood that the work was leaving the center, and who positioned themselves to ride the wave that goes everywhere else.

Stay small and distributed. Stay sovereign over your own compute and your own data. The capex titans figuring this out the hard way is just the next chapter of an old story that anyone who reads infrastructure history could have seen coming a decade ago.

Be good to each other. And don’t get caught holding last year’s hardware.

In order for artificial intelligence (AI) to work right within the law and thrive in the face of growing challenges, it needs to integrate an enterprise blockchain system that ensures data input quality and ownership—allowing it to keep data safe while also guaranteeing the immutability of data. Check out CoinGeek’s coverage on this emerging tech to learn more why Enterprise blockchain will be the backbone of AI.

This opinion piece is published to encourage discussion. The author’s views are their own and do not constitute legal, procurement, or policy advice, nor do they represent the positions of CoinGeek or its partners.

Watch: Demonstrating the potential of blockchain’s fusion with AI

Be the first to comment