TL;DR:

- BlackRock’s BUIDL fund records over $3.1 billion in assets under management and has distributed more than $100 million in cumulative dividends.

- Approximately 10% of tokenized real-world assets are actively deployed within DeFi protocols today.

- The Centrifuge platform surpassed $1.5 billion in total value locked following institutional traction of its JAAA and JTRSY products.

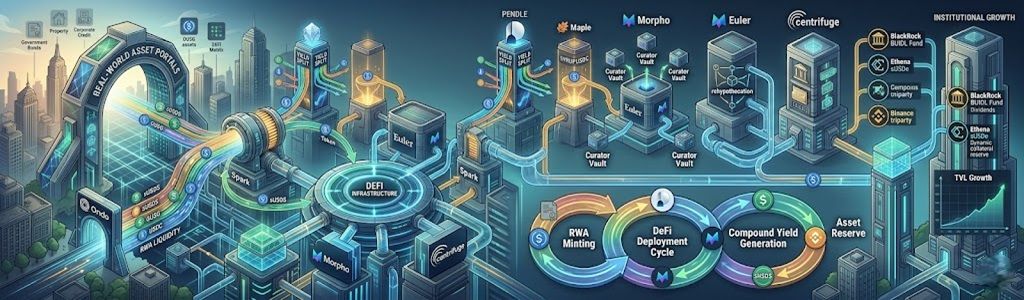

The tokenized RWA market is reshaping capital dynamics within the DeFi ecosystem by developing leverage structures that connect traditional finance with the crypto environment.

Generally, crypto-native communities are not attracted to real-world asset tokenization. Some of these instruments sat idle, earning modest treasury yields without interacting with decentralized infrastructure.

Recent market data indicates that access limitations restrict liquidity, but the technical architecture of leading protocols points to deeper integration.

Collateral Expansion and Financial Derivatives

Despite having billions of dollars under management, BUIDL’s direct DeFi-active total value locked sits at $18.9 million due to permissioning restrictions. However, the fund’s reach is manifested through derivative products. The USDtb coin maintains BUIDL as its primary reserve, while OUSG uses this same underlying instrument to generate yields for its users. The asset functions simultaneously as collateral in the triparty custody services of Binance, Deribit, and Crypto.com.

An analysis by specialist Kaff on his X account indicates that this movement is equivalent to the rebuilding of the repo market in DeFi. The documented technical process begins with the issuance of a yield-bearing real-world asset, later splitting said benefit on the Pendle platform.

► RWA Loops In DeFi Thesis#RWA don’t usually get much CT mindshare because it’s boring. I keep yapping about RWAs because I enjoy that yield every day.

Only ~10% of tokenized assets are locked in DeFi today but things will def change once people realize these assets don’t… pic.twitter.com/fV4ihAKbIn

— Kaff 📊 (@Kaffchad) May 26, 2026

The principal token is subsequently deposited as collateral in Morpho, Euler, or Aave. With these funds, borrowed stablecoins are used to purchase more yield-bearing collateral, restarting the operational cycle.

Yield Protocol Infrastructure

Ondo Finance integrates Wall Street assets for use as commercial margin in perpetual trading venues and DeFi platforms. Meanwhile, Maple Finance introduced verified institutional borrower demand onto the blockchain through syrupUSDC, a product incorporated into Morpho, Pendle, Kamino, and Revolut.

Morpho’s architecture operates similarly to a prime broker for this suite of applications. Its isolated markets allow financial institutions to deploy custom credit environments without assuming the liquidity risks of a shared pool.

Pendle transformed idle assets into tradeable fixed-income instruments. Its principal tokens now serve as the foundation for interest rate arbitrage operations across the ecosystem.

In parallel, platforms like Apyx and Saturn Credit channel Strategy’s dividend yield directly onto the blockchain, wrapping them in Pendle and distributing them through Morpho. Euler’s EVC architecture complements this design by allowing rehypothecation and the movement of collateral between different security vaults.

Finally, Spark stands out as one of the largest capital allocators in this segment, with the sUSDS module backing billions in reserves. Its Tokenization Grand Prix initiative mobilizes hundreds of millions of dollars toward Centrifuge products, while Ethena demonstrates that synthetic dollars can act as productive collateral in these financial circuits.

Be the first to comment