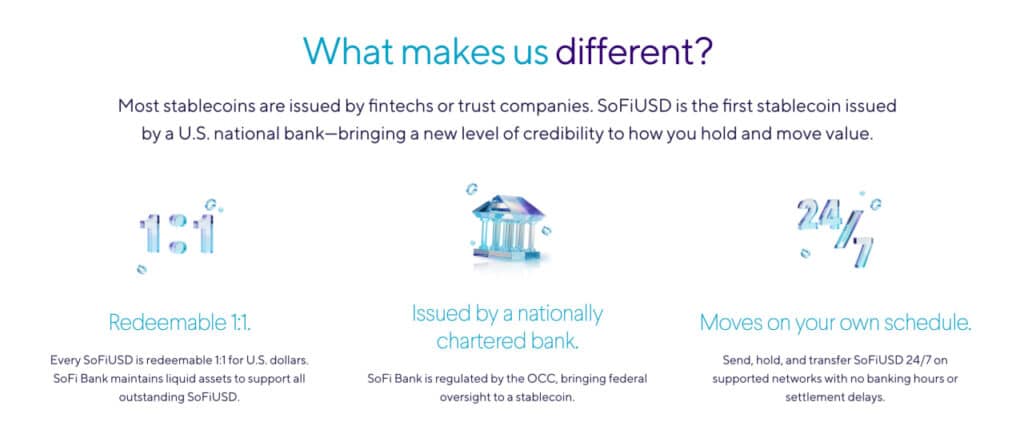

In the latest Solana news, SOFIUSD, a dollar-pegged stablecoin launched by SoFi, a publicly traded, bank-chartered fintech with 15.4 million members, on both the Ethereum and Solana networks in early 2026.

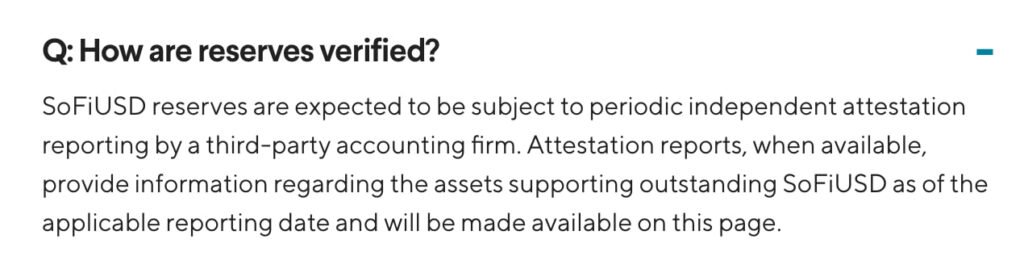

Every token is backed 1:1 by a reserve portfolio consisting of 85% short-term U.S. Treasury bills and 15% cash held at FDIC-insured institutions, with those reserves verified monthly by Deloitte and held in segregated accounts at the Federal Reserve Bank of San Francisco.

Here is the central tension this article unpacks: the word “regulated” gets attached to a lot of financial products, but for retail investors considering SOFIUSD, what that label actually means in practice, what it protects, what it does not protect, and how it compares to existing options like USDC or USDT, is worth understanding clearly before you move a single dollar in.

Say “hi” to SoFiUSD (SoFiD) 👋

The first stablecoin issued by a U.S. national bank and redeemable 1:1 for cash or cash equivalents. Rolling out now, it’s built for how money moves today: fast, flexible, 24/7. pic.twitter.com/I0eHIxDR50

— SoFi (@SoFi) May 27, 2026

DISCOVER: The Next 1000x Crypto Gem Before It Lists on Binance

Solana News: What is SOFIUSD? The Plain-English Explanation

Think of SOFIUSD like a digital claim ticket for a real dollar sitting in a government-supervised vault. When you hold one SOFIUSD token, SoFi is required by law to hold one dollar’s worth of U.S. Treasury-backed assets on your behalf.

The token itself lives on a blockchain, either Ethereum or Solana, but the value behind it never leaves regulated financial infrastructure.

The 1:1 peg means that one SOFIUSD should always be redeemable for one US dollar, and the Stablecoin Transparency and Accountability Act signed into law in late 2025 legally requires SoFi to honor that redemption within two business days.

That is meaningfully different from an algorithmic stablecoin, which tries to maintain its peg through code and market incentives rather than actual dollar reserves, a model that collapsed catastrophically with TerraUSD in 2022.

The U.S. Treasury-backed reserve structure also distinguishes SOFIUSD from earlier stablecoins that kept their backing opaque. Tether, the issuer behind USDT, spent years facing questions about whether its reserves were real and fully liquid. SoFi publishes its reserve composition daily on its website, which is a standard entirely different from the one used by other banks.

On the technical side, SOFIUSD is issued as an ERC-20 token on Ethereum for institutional-grade use, and as an SPL token on Solana for fast, low-cost retail transactions, and Solana’s Q1 2026 network data shows why that chain matters for payment-speed stablecoin use cases.

DISCOVER: Best Meme Coin ICOs to Invest in 2026

What Does ‘Regulated’ Status Actually Mean for Retail Investors?

The word “regulated” does real work here, but only if you understand what it covers. SoFi is supervised by the Office of the Comptroller of the Currency as a nationally chartered bank, the same regulatory category as traditional banks – which means it already meets capital requirements and consumer protection standards that most crypto-native stablecoin issuers have spent years trying to replicate through state-by-state money transmitter licenses.

In concrete terms, the regulated stablecoin structure provides three meaningful protections that an unregulated or offshore issuer cannot offer:

Reserve transparency: Monthly SOC 2 Type II attestations by Deloitte verify that the reserves backing every SOFIUSD token actually exist and are composed as stated. You are not trusting a press release; you are trusting an audited report from a registered accounting firm.

Redemption guarantee: The Stablecoin Transparency and Accountability Act requires a full redemption within two business days. SoFi processes these through the same ACH and wire systems it already uses for regular withdrawals, so the infrastructure exists and is tested.

Segregated reserves: The assets backing SOFIUSD are held in segregated accounts, meaning they are legally separated from SoFi’s operating capital. If SoFi faced financial difficulty, those reserves would not be available to creditors; they exist solely to back the tokens.

What regulated status does NOT guarantee is equally important to name. SOFIUSD is not FDIC insured, SoFi’s own disclosures say so explicitly. It does not eliminate smart contract risk, where a bug in the token’s code could theoretically be exploited.

It does not protect against chain-level disruptions on Ethereum or Solana. And the 4.2% APY promotional yield offered during launch is funded by Treasury reserve income, which means it can change as interest rate conditions shift. Regulation raises the floor; it does not remove every ceiling.

For additional context on why regulated status matters in the broader crypto landscape, the ARMA Bill explainer covers how U.S. regulatory frameworks are reshaping the way digital assets are classified and supervised, relevant background for anyone trying to understand why a bank charter changes the risk profile of a stablecoin issuer.

Follow 99Bitcoins on X For the Latest Market Updates and Subscribe on YouTube For Daily Expert Market Analysis.

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

90hr+

Weekly Research

100k+

Monthly readers

50+

Expert contributors

2000+

Crypto Projects Reviewed

Follow 99Bitcoins on your Google News Feed

Get the latest updates, trends, and insights delivered straight to your fingertips. Subscribe now!

Be the first to comment