Bitcoin’s options market has grown too large to ignore. What that signals about who is now participating in crypto, and why, matters more than the numbers alone.

Crypto markets are no stranger to sharp drawdowns. As Bitcoin fell roughly 50% from its October 2025 peak to a low of around $60,000 in February, however, one aspect was different from previous cycles. Beyond the usual forced liquidations and directional panic, capital also moved en masse into instruments designed to manage the decline — first through downside protection, then through renewed upside exposure at defined risk as prices stabilised.

Those instruments were, of course, options — derivatives that have long been central to professional risk management in traditional finance. Their rapid growth in crypto over the past two years isn’t simply a story of a new product gaining traction. Instead, it points to a change in who’s participating in these markets and what they require from them: not just directional exposure, but the ability to hedge, transfer and structure risk precisely.

In that sense, the rise of options is one of the clearest signs yet of crypto’s growing institutionalisation — and of a market finally coming of age.

What Options Are and Why They Matter

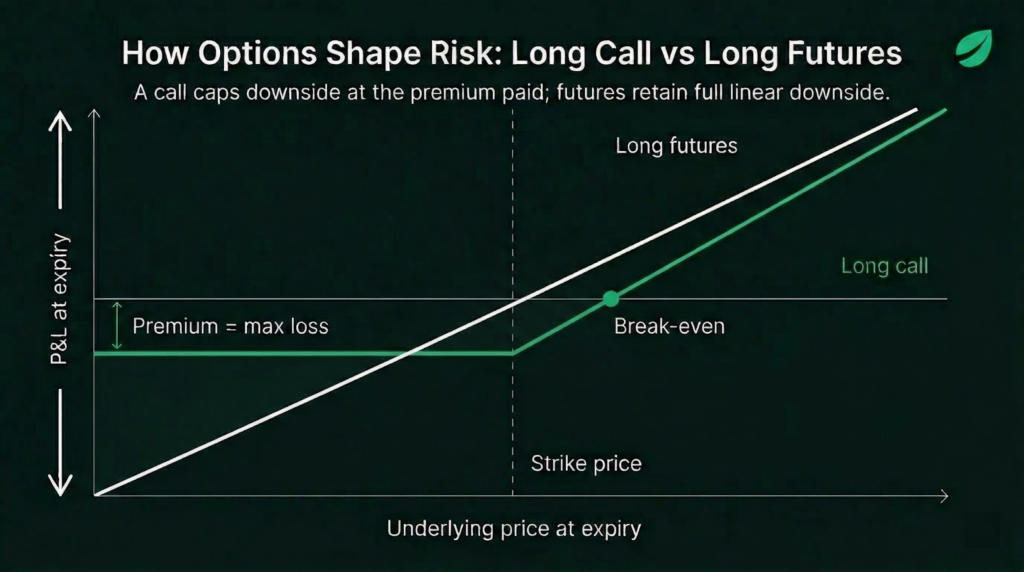

A call option gives the buyer the right, but not the obligation, to purchase an asset at a fixed price before a set date. A put gives the right to sell, with the buyer paying a premium upfront. If the market moves against them, that premium acts as an upper limit on their loss.

That asymmetry is what makes options categorically different from spot and futures. Spot contracts provide exposure. Futures give linear leveraged exposure. Options give non-linear exposure, i.e. the ability to shape a payoff profile in advance, defining what a position returns under different market conditions.

The practical consequences are significant. A fund holding Bitcoin, for example, can buy puts to cap downside without liquidating the underlying asset. A miner can lock in a price floor for future production without surrendering upside if Bitcoin rallies. A treasury desk can sell calls against existing holdings to generate yield in a flat market. A volatility trader can structure a payoff around an expected range of price movement without taking a directional view at all.

What options introduce, in short, is discretion.

In a spot-dominated market, participants mostly face a binary choice: either hold the risk or exit it. Options allow participants to retain exposure while rearranging the associated risks. For institutions managing significant capital, that’s the important difference between being able to hold a Bitcoin allocation through volatility and being forced to exit it at a loss.

What makes this convergence rather than simply more sophisticated speculation is not the presence of options alone, but the purposes they serve. In mature financial markets, options are used less for directional bets than for hedging inventories, managing treasury exposure, expressing views on volatility and constructing defined-risk strategies within formal portfolio constraints. As those same functions become routine in Bitcoin markets, the asset begins to fit more naturally inside the operating logic of traditional capital, rather than existing outside it.

What the Data Shows

The growth of Bitcoin and crypto options is no longer a background story. Deribit, the dominant crypto-native options venue, recorded $1.185 trillion in trading volume in 2024 — a 95% increase year-on-year — with options alone surging 99%, accounting for $743 billion. In 2025 it was acquired for $2.9 billion, one of the largest deals in crypto history, a price reflecting how seriously established players now view options market access. Roughly 80% of Deribit’s volume and open interest is generated by institutional participants, a composition that speaks directly to who is driving the growth of crypto options.

The growth has not been confined to crypto-native venues. The launch of options on BlackRock’s spot Bitcoin ETF on November 19, 2024 was significant, generating$1.9 billion in notional exposure on its first day of trading alone. Within a year, IBIT options hadentered the top ten US options markets by active contracts, surpassing the SPDR Gold ETF, and accounted for roughly 52% of total bitcoin options open interest.

That speed of adoption reflects pre-existing demand from ETF holders in custodied accounts with existing brokerage infrastructure, for whom options on a product they already owned were immediately useful.

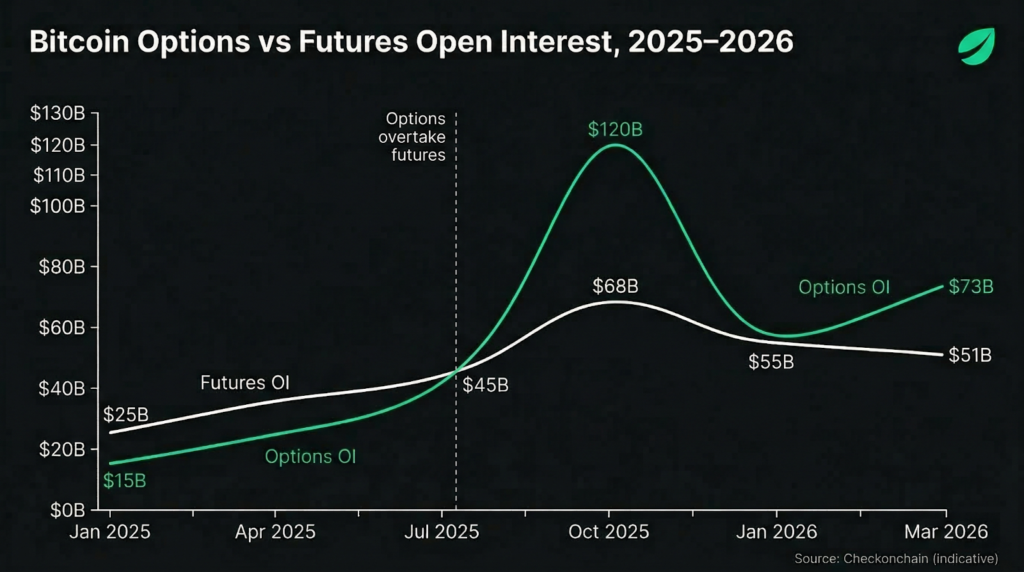

The most telling structural signal is the shift in overall open interest. According to Checkonchain data, bitcoin options open interest moved above futures open interest in July 2025, reaching roughly $73 billion against futures’ $50 billion by mid-March 2026. What is most interesting is not the crossover itself but that options open interest has remained above futures open interest throughout one of Bitcoin’s most volatile stretches since 2022.

How Options May Be Reshaping Bitcoin’s Market Structure

The growth of options is not only a sign of a more sophisticated participant base — it may be actively changing how Bitcoin itself behaves.

When a large options market exists, the dealers who intermediate that flow are required to hedge their exposure dynamically in spot and futures markets. That hedging creates mechanical pressure near heavily populated strikes and expiry windows that can compress volatility in both directions, cushioning sell-offs but also tempering rallies. A large options market does not merely sit on top of the asset. It changes how the asset trades.

The evidence is suggestive rather than conclusive. The current cycle’s roughly 50% drawdown from Bitcoin’s $126,000 peak has been materially shallower than the 78% decline that followed the 2021 high. Also absent, so far, is the kind of cascading structural failure that characterised the 2022 downturn. A larger, more structurally sticky options market is a plausible part of that explanation.

The infrastructure supporting that market has developed primarily through centralised venues, mainly due to the structural demands of institutions. Professional participants need deep liquidity across strikes and expiries, portfolio margining, regulatory alignment and integration with existing account and compliance workflows. Bitfinex’s partnership with Thalex is one such example, giving verified Bitfinex Derivatives users access to USDt-settled options, portfolio margining and a range of expiries through a full-access integration.

On-chain options protocols have nonetheless also expanded, a November 2025 report from Delphi Digital noting decentralised platforms having grown their market share from roughly 2% to over 10% in two years. Institutional flow continues to remain concentrated, however, where those operational requirements are currently best met.

Risk That Can Be Shaped, Not Just Endured

The deeper significance of the options market’s growth lies in what it suggests about crypto’s increasing maturity as a whole.

Spot markets made Bitcoin accessible and futures made it tradeable at scale. Options are making it governable, giving participants the ability to measure risk, purchase protection against it, hedge it, distribute it and reprice it, rather than simply endure its volatility.

This is important because it allows Bitcoin financial markets to deepen. A market where participants can only take exposure or avoid it is fundamentally limited. A market where risk can be sliced, structured, hedged and transferred is one that can support a much broader range of participants and strategies, including the institutional capital that crypto has spent a decade trying to attract. At the furthest end of the institutional spectrum, Bitcoin volatility is increasingly treated as a macro signal in its own right — a reflection of global risk appetite that extends well beyond Bitcoin itself.

That doesn’t mean Bitcoin has been tamed. But it does mean it is becoming more financeable — and that is monumental.

Be the first to comment