Can Sandisk Go Above $1,500 Next Week?

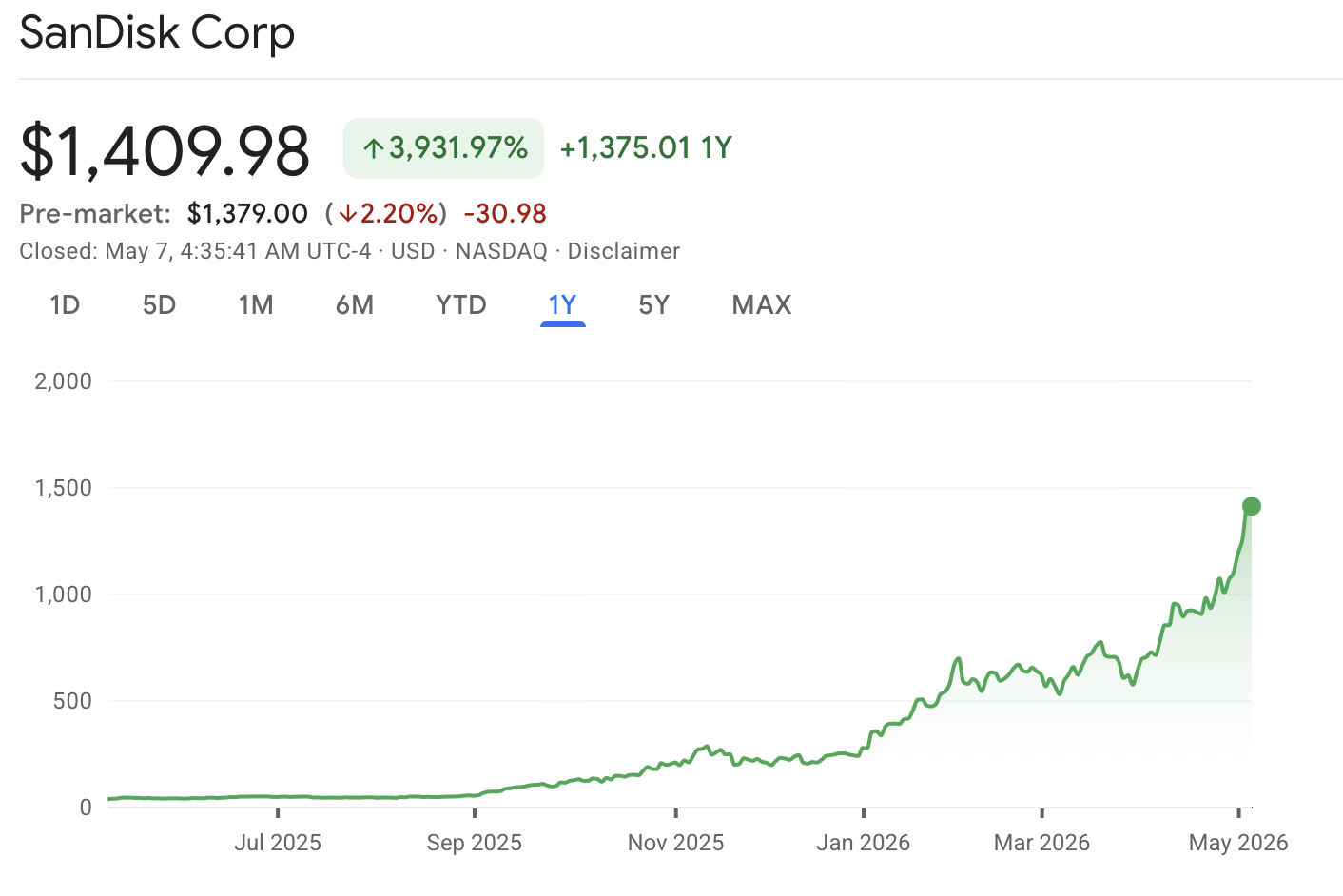

Sandisk enters next week within striking distance of $1,500 after one of the sharpest large-cap rallies in U.S. technology. The memory-chip company recently traded near $1,410, with a market value above $220 billion, after touching fresh record territory during its latest AI-driven surge.

A break above $1,500 next week would likely need the same forces that drove the latest rally: strong AI infrastructure demand, index-linked buying after Nasdaq-100 inclusion, tight NAND supply, and continued confidence in Sandisk’s long-term customer agreements. The stock has already shown it can move quickly after earnings, but a run this steep also leaves room for profit-taking if AI memory names cool or if investors rotate away from high-momentum semiconductor trades.

Over the past year, Sandisk has jumped from roughly $33 to more than $1,400, an almost 4,000% move that turned the stock into one of the most dramatic AI-linked winners in the market. The rally accelerated after the company’s earnings breakout, stronger NAND pricing, tighter memory supply, and rising demand from data-center customers building AI infrastructure.

Sandisk completed its separation from Western Digital on Feb. 24, 2025, returning to Nasdaq as an independent flash storage company. Less than 15 months later, the stock has become one of the fastest-rising large-cap technology names in the market. The next-week setup now centers on whether buyers can push through $1,500 or whether the stock needs to consolidate after turning AI storage demand into one of the market’s strongest momentum trades.

Nasdaq-100 Inclusion Added Index Demand

The timing of Sandisk’s Nasdaq-100 entry added another layer to the trade. Nasdaq announced that Sandisk would join the Nasdaq-100 before the market opened on April 20, replacing Atlassian. The inclusion forced index-linked funds and ETFs tracking the Nasdaq-100 to add exposure, giving the stock a mechanical demand channel on top of the AI-driven earnings story.

That index effect arrived while investors were already chasing companies tied to AI infrastructure. The strongest demand has moved beyond GPU makers into memory, storage, networking, power, and data-center capacity. Sandisk sits directly inside that stack because AI workloads require high-performance NAND flash, SSD capacity, and enterprise storage systems to move and store massive training, inference, and retrieval data.

A recent AI chip supercycle story captured the same broad rotation: capital is flowing into companies that can support the physical buildout behind artificial intelligence, not only the model developers and GPU leaders at the top of the trade.

Earnings And Supply Deals Fueled The Breakout

Sandisk’s latest results gave bulls more than a momentum chart. The company reported fiscal third-quarter revenue of $5.95 billion, up 97% sequentially and above guidance, with GAAP net income of $3.62 billion and non-GAAP diluted earnings of $23.41 per share. Datacenter revenue rose 233%, helped by a mix shift toward higher-value customers and stronger pricing.

The company also announced a $6 billion share repurchase program after repaying debt. More importantly for investors, Sandisk secured long-term supply agreements with firm financial commitments, including three new business-model partnerships worth at least $42 billion. Those contracts can help reduce some of the volatility that has historically defined memory-chip cycles by locking in customer commitments and pricing structures.

The market is rewarding that visibility. Memory and storage businesses normally face boom-bust pricing pressure when new capacity catches up with demand. AI data centers have changed that balance for now, with hyperscale customers competing for storage capacity while inventories remain tight.

Why This Matters Beyond Traditional Stocks

Sandisk’s rally also connects to crypto’s capital-market backdrop. AI infrastructure has been one of the strongest equity themes of the year, pulling retail and institutional flows toward chip, memory, and data-center names while crypto ETF demand remains more concentrated in Bitcoin. A recent AI capex and ETF flow story showed how semiconductor-linked products have captured a different intensity of investor demand than broader crypto funds.

The tokenized-stock angle is also growing. As more equities move onto onchain rails through tokenized stock products, high-volatility names such as Sandisk, Nvidia, Tesla, and MicroStrategy become natural targets for platforms trying to bring traditional market exposure into crypto trading environments. Recent tokenized-equity launches on Solana and centralized exchanges show that the gap between stock momentum and crypto market infrastructure is narrowing.

Sandisk’s breakout is not risk-free. The valuation now assumes that AI storage demand, NAND pricing, and long-term customer commitments can hold up through a larger capacity cycle. If supply catches up too quickly or hyperscale customers slow capex, the same operating leverage that lifted earnings can pressure margins. A move above $1,500 next week would strengthen the AI memory trade, while a pullback would test whether investors still treat Sandisk as a core infrastructure winner after one of the fastest large-cap rallies of the year.

Be the first to comment