Key Takeaways

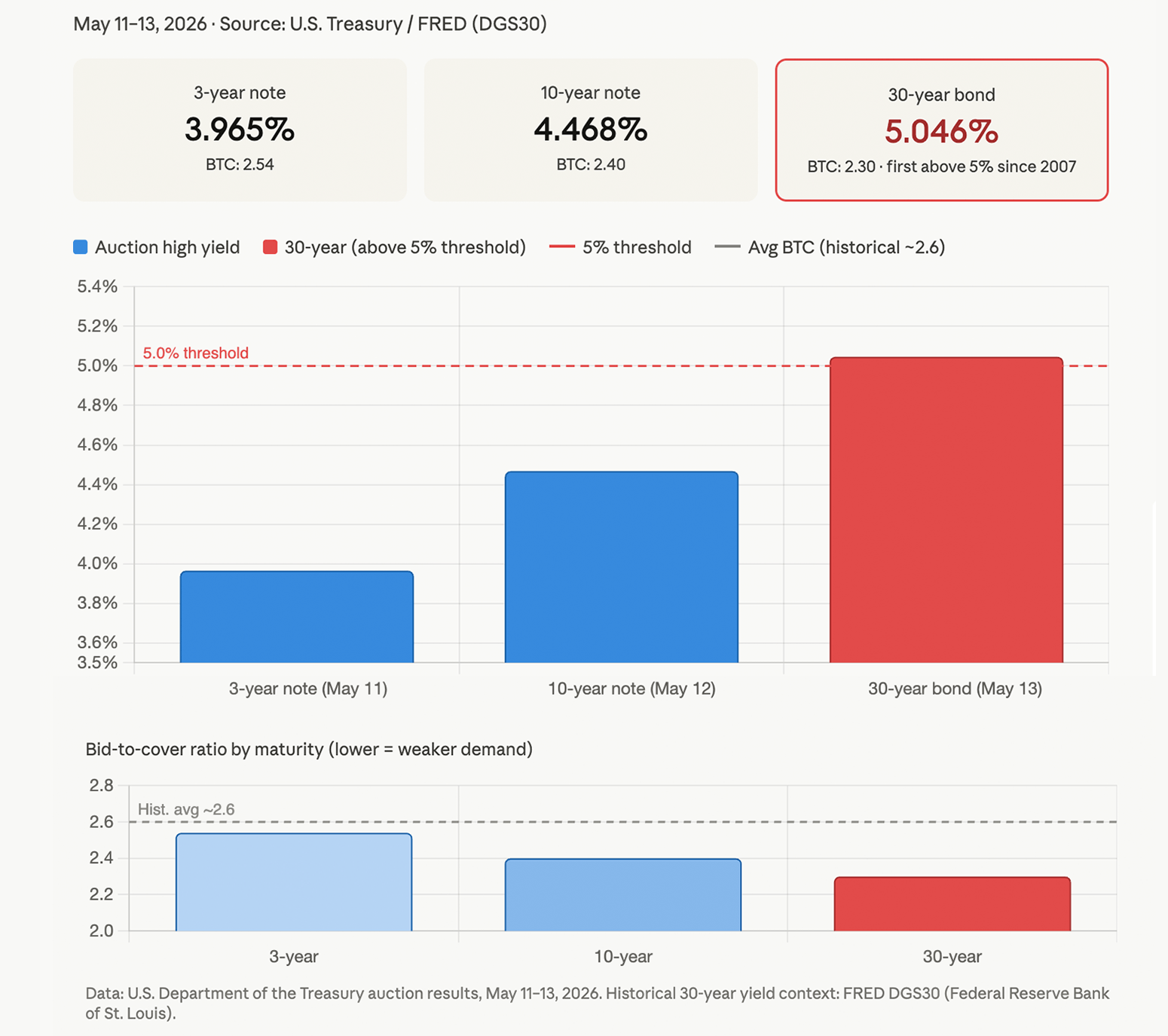

- The U.S. Treasury sold $125B in new debt May 11-13, with the 30-year bond clearing at 5.046%, the highest since 2007.

- Bid-to-cover ratios across all three auctions fell below 2.55, signaling weakening investor appetite for long-dated U.S. debt.

- Rising 30-year yields toward 5.1% threaten to push mortgage rates and corporate borrowing costs higher in the weeks ahead.

Investors Push 30-Year Treasury Yield Above 5% as U.S. Auction Demand Falls to 2007 Lows

The three auctions, covering 3-year notes, 10-year notes, and 30-year bonds, settled May 15 against a backdrop that few fixed-income investors would call comfortable. April CPI and PPI data both came in hotter than expected. Oil crossed $100 per barrel on Middle East tensions tied to Iran. And the federal government kept borrowing at a pace that gives bondholders little room to relax.

The results were unambiguous. Investors wanted more yield to show up.

On May 11, the Treasury sold $58 billion in 3-year notes at a high yield of 3.965%. The bid-to-cover ratio came in at 2.54, with indirect bidders, typically foreign institutions and central banks, absorbing roughly 63% of competitive awards. Market participants flagged the result as soft, requiring a pricing concession to clear.

The 10-year auction on May 12 drew sharper concern. The Treasury placed $42 billion at a high yield of 4.468%, with a bid-to-cover of 2.40. The auction tailed pre-auction levels by roughly 0.4 basis points or more, meaning buyers demanded a higher yield than traders had priced in beforehand. That outcome pushed the 10-year note yield into the 4.48 to 4.59% range in spot trading after results were published.

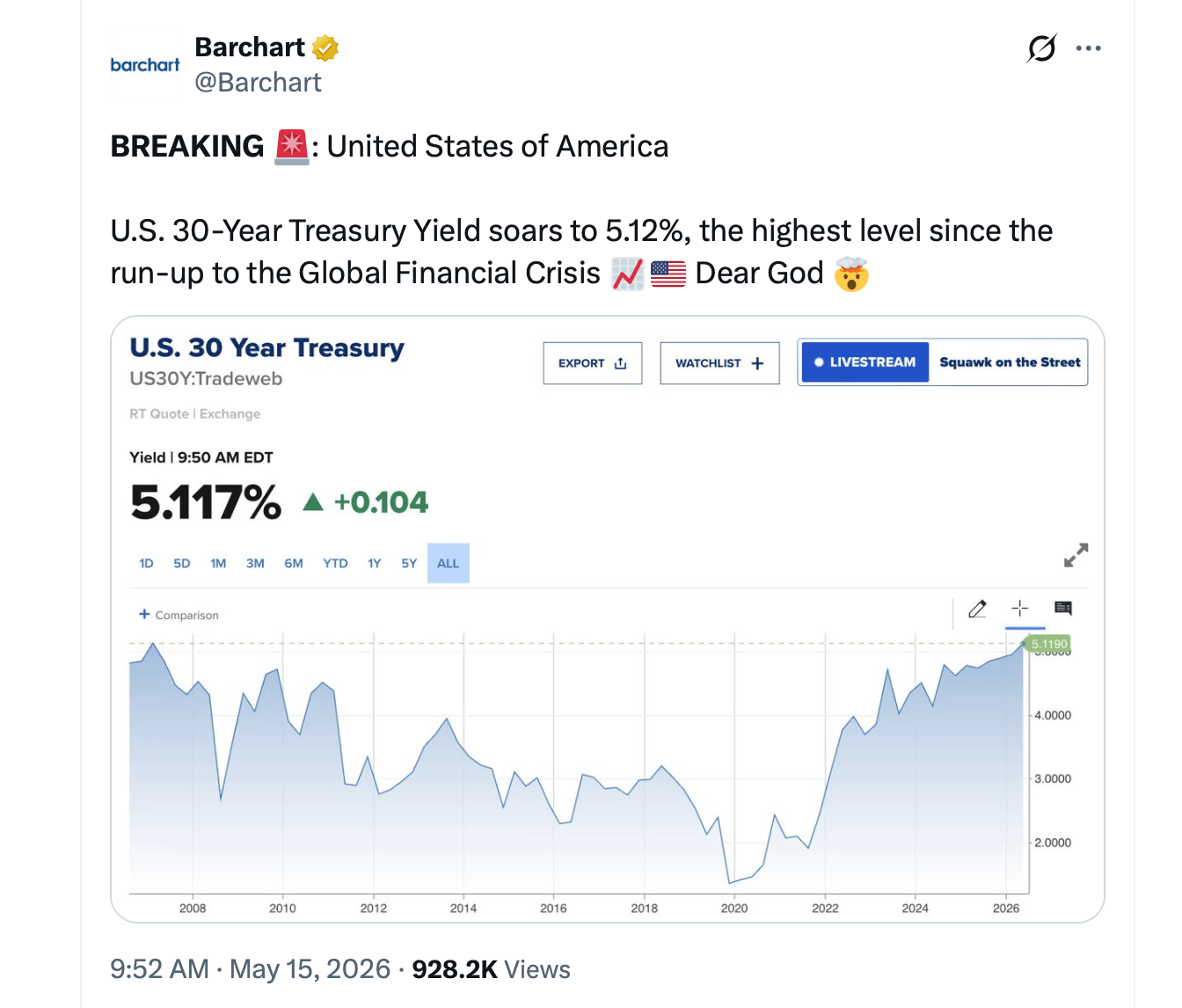

The 30-year auction on May 13 carried the week’s most notable signal. The Treasury sold $25 billion at a high yield of 5.046% with a coupon set at 5.000%. That marked the first time since August 2007 that a 30-year bond cleared at or above 5%. The bid-to-cover landed at 2.30, the weakest of the three auctions. The result pushed 30-year yields toward 5.1% in the days following settlement.

Indirect bidders provided the clearest sign of continued overseas engagement, taking roughly 66.6% of competitive awards in the 30-year sale. But overall participation lagged the levels seen before geopolitical tensions intensified earlier this year. Primary dealers, which are required to bid, absorbed a smaller share than in recent auctions, suggesting limited conviction from domestic institutional buyers.

The pattern across the week was consistent. Each auction tailed expectations. Each bid-to-cover came in below recent historical averages that have typically run above 2.5 to 2.6. Each result, when published, pushed yields higher.

For U.S. households and businesses, the implications are direct. Mortgage rates, auto loans, and corporate bonds all price off Treasury yields. A 30-year government bond clearing above 5% means borrowing costs across the economy face continued upward pressure.

For the federal government, the math compounds quickly. With national debt in the tens of trillions, paying higher yields on each new issuance widens the interest expense. That expense competes with every other line in the federal budget.

Equity markets have historically treated a 30-year yield above 5% as a warning. Higher risk-free rates make long-duration assets, particularly growth stocks, worth less in present-value terms. That dynamic has not gone unnoticed on trading desks in May.

The Federal Reserve faces its own challenge. If inflation remains elevated, driven partly by energy costs tied to geopolitical disruption, rate cuts become harder to justify. Long-term yields embedding higher inflation expectations signal that markets are not counting on a quick pivot.

For now, U.S. Treasuries remain liquid and functional. No auction has failed. But investors are pricing in caution at the long end of the curve, and each successive weak result reinforces the pressure on policymakers to respond to inflation data before borrowing costs move further.

The next major data points, including May CPI and any Fed communications, will determine whether this week’s auction results represent a plateau or a floor.

Be the first to comment