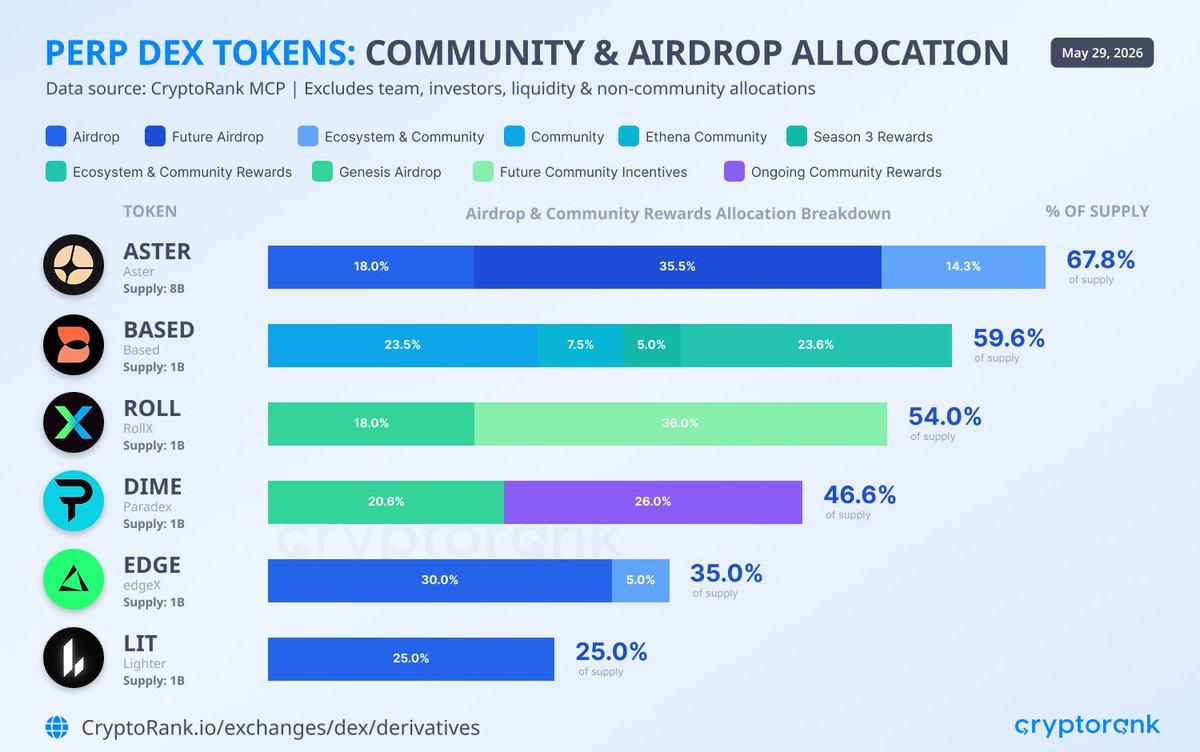

Aster DEX allocated 67.8% of total supply to community rewards and airdrops – more than any other perp DEX launched in the past year.

Key Takeaways:

When a crypto project launches a token, one of the first decisions it makes is who gets what. That decision, usually buried in a tokenomics document most people never read, determines more about a token’s long-term price behavior than almost anything else. It determines who will eventually sell, when they’ll sell, and how much pressure hits the market when they do.

The standard model in crypto has been straightforward and mostly bad for retail: raise from VCs at a cheap price, allocate a meaningful chunk to the team, give the community something that looks generous but isn’t, list the token, and let the early investors gradually distribute into retail demand. Arthur Hayes described this plainly, the day of the token generation event is often the highest price the token will ever see, because from that point forward there’s a queue of early buyers with locked tokens waiting to exit into anyone willing to buy.

The data from CryptoRank MCP on perp DEX tokens launched over the past year shows what happens when projects try to run a different playbook.

Why community allocation matters mechanically

The core idea is simple. If you give 67.8% of your token supply to users through airdrops, ecosystem rewards, and community incentives, those tokens go to people who earned them by using the product. They didn’t buy at a seed round for fractions of a cent. They have no lockup schedule enforced by a fund’s LP agreements. They’re retail participants who got tokens for trading, providing liquidity, or being early adopters.

That changes the sell pressure dynamic completely. Instead of a concentrated group of professional sellers, VCs with fiduciary duties to their LPs, team members waiting for vesting cliffs, you have a widely distributed group of ordinary holders with different cost bases, different time horizons, and different reasons to hold or sell. Some will dump immediately. Many will hold. The selling gets spread across thousands of wallets rather than concentrated in a handful of early investors all hitting the same unlock date at the same time.

It doesn’t eliminate sell pressure. It distributes it differently. And distributed selling tends to be less violent than coordinated institutional exits.

What the numbers show

According to CryptoRank data, Aster leads the ranking at 67.8%, more than two thirds of its 8 billion total supply directed toward community. The structure splits into three buckets: 18% in an initial airdrop that went out at launch, 35.5% sitting in an ecosystem and community fund that gets distributed over time based on protocol activity, and 14.3% in ongoing community rewards that keeps flowing to active users. The ongoing nature of those last two buckets is important. It means the protocol has a sustained mechanism for attracting and retaining users rather than a one-time airdrop that creates a spike and a dump.

Based comes second at 59.6% with the most layered structure of any project on the list. It runs four separate community channels simultaneously: 23.5% in an initial airdrop, 7.5% reserved for a future airdrop not yet distributed, 5% in ecosystem development, and 23.6% in ongoing community rewards. The future airdrop reserve is particularly interesting, it gives the team flexibility to reward future users rather than only those who were early, which reduces the advantage of being first and theoretically broadens participation over time.

Roll at 54% took a different approach. 18% went out as a genesis airdrop and 36% sits in a future community incentives pool. That 36% is the largest single community-directed pool in the entire dataset, bigger than anything Aster or Based reserved for any single bucket. The question with a pool that size is how it gets distributed. If it’s tied to genuine protocol usage and trading activity it’s a powerful long-term user acquisition tool. If it’s poorly designed it becomes a farming target that attracts mercenary capital with no intention of staying.

Dime at 46.6% runs a 20.6% genesis airdrop alongside 26% in ongoing community rewards, a balance that acknowledges early users while keeping a sustained flow going to future participants. Edge at 35% is more conservative, putting 30% into an initial airdrop and 5% into a future airdrop, with the bulk of the community allocation going out upfront rather than over time. Lit at 25% is the most restrained on the list, a single 25% airdrop with nothing reserved for future community distribution, which raises the question of what mechanism keeps users engaged once that initial distribution is done.

Why perp DEXes specifically are doing this

Perpetual futures DEXes have a specific competitive dynamic that makes tokenomics more important than in other sectors. The product itself is a commodity, you can trade perpetuals on dozens of platforms. The fees are similar, the assets are the same, the leverage options are nearly identical. What differentiates one perp DEX from another, especially in the early months, is almost entirely about incentives. Who pays traders to use the platform? Who rewards liquidity providers? Who makes early adopters feel like they got something real for showing up first?

A 67.8% community allocation isn’t altruism. It’s a user acquisition strategy expressed in tokenomics. Aster is essentially saying: we will spend the majority of our token supply buying users, building loyalty, and creating a holder base that has a direct financial stake in the protocol’s success. Every token that goes to a community member is a token that could have gone to a VC or a team member. The choice to route it toward users is both a competitive decision and a statement about what kind of holder base the project wants.

What this data doesn’t answer

The chart only shows one side of the cap table. The community percentages are the visible part. What the team kept, what went to investors, and at what prices those parties entered are not shown here. A project could allocate as much as Aster to community and still have a VC overhang that dominates price action if the remaining part is concentrated and cheap enough. The community allocation is a necessary condition for a healthier token structur, it’s not sufficient on its own.

The supply sizes also differ in ways the percentages flatten. Aster’s 8 billion token supply at 67.8% represents a fundamentally different absolute quantity than Roll’s 1 billion supply at 54%. If Aster’s price per token reflects the dilution of a larger supply, community members receiving tokens in percentage terms may not be receiving equivalent value. The mechanism matters as much as the headline number.

Three of the six projects on this list put more than half their total supply in community hands. That’s a meaningful shift from the standard model. Whether it produces better long-term outcomes for token holders is a question the market will answer as these protocols mature and their vesting schedules play out. But the structural choice is visible in the data. These projects decided early on who their primary stakeholder is. That decision rarely gets reversed.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice. Coindoo.com does not endorse or recommend any specific investment strategy or cryptocurrency. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP.

Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem.

To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem.

His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.

Be the first to comment