Bitcoin retail inflows have hit record lows on Binance, while ETF holders are aggressively redeeming assets. Is this a structural market warning or a classic contrarian bottom signal?

Key Takeaways

- Retail inflows to Binance hit a record low of 329 BTC per day.

- That’s roughly 8x below the 2021 average and 11x below 2018.

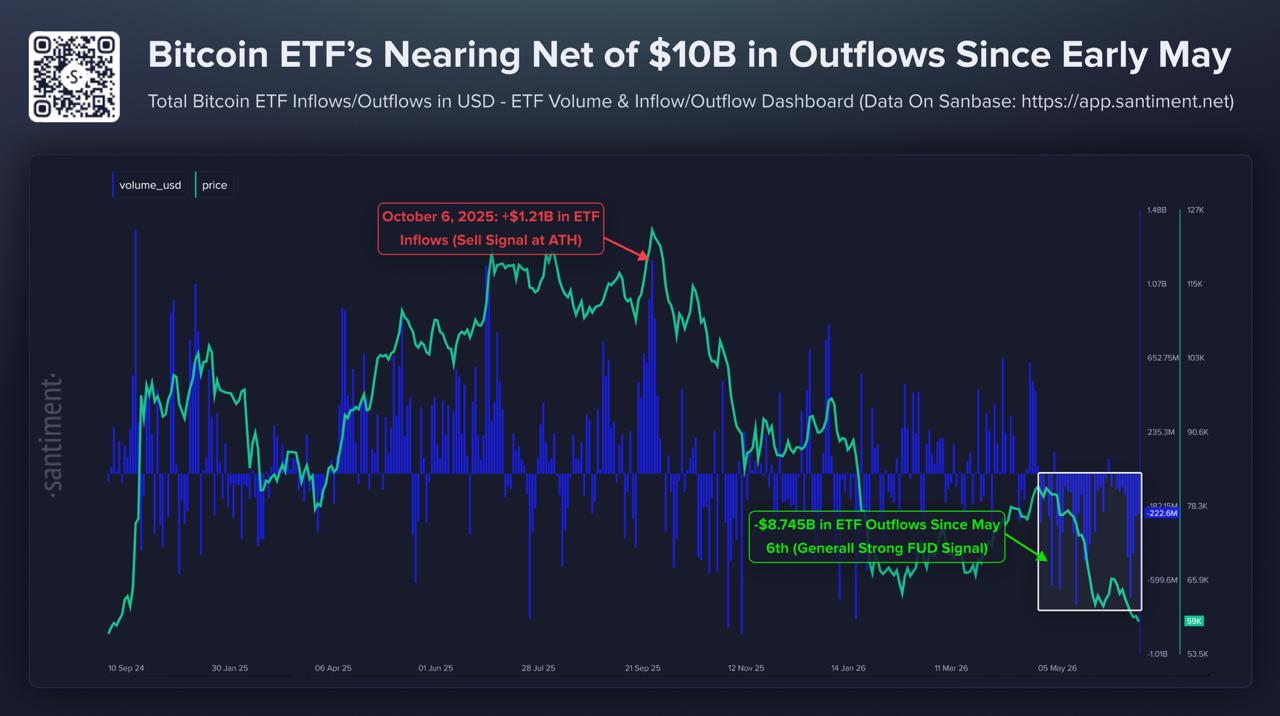

- Bitcoin ETFs have seen about $8.48 billion in net outflows since May 6.

- Both point to the crowd exiting, but neither is a timing signal.

Retail Never Showed Up This Cycle

Data from CryptoQuant shared by analyst Darkfost, tracking Binance inflows under 1 BTC, a proxy for retail, against price since 2018. According to the analyst, retail inflows now average 329 BTC per day, the lowest in the exchange’s history. The historical contrast is the whole point:

| Period | Retail Inflows (avg/day) |

|---|---|

| 2018 cycle | 3,700 BTC |

| 2021 peak | 2,690 BTC |

| Now | 329 BTC |

That’s roughly an 8x collapse from the 2021 average and 11x from 2018, which saw a single-day record of 10,400 BTC. The telling detail: the 30-day average that spiked in every prior cycle (2018, 2021, 2023) flatlined near the bottom of its range through 2025-2026, even as Bitcoin ran above $100K. Every price top this cycle failed to trigger a retail spike. The cohort simply didn’t turn up.

Darkfost’s Explanation

Darkfost offers several possible reasons, framed as his analysis. Retail may have chased exposure elsewhere this cycle, in altcoins or other assets. Spot Bitcoin ETFs may have captured investors and pulled them out of on-exchange activity into a wrapped vehicle. And some retail may simply be holding longer-term or waiting for better performance. His broader framing is that this cohort could be “going extinct” on Binance, with the market’s makeup shifting toward institutionalization.

The ETF Outflows Tell a Parallel Story

The wrapped-exposure crowd is leaving too. According to Santiment, Bitcoin ETFs have combined for about $8.74 billion in net outflows since May 6, approaching the $10 billion mark. Santiment’s read is explicitly contrarian: it treats sustained outflows as a sentiment signal, where price tends to move opposite the crowd’s expectations over time, rather than a mechanical predictor of further downside. The longer the outflow streak, in their view, the more it reflects fear and capitulation than a fresh reason to sell.

Their historical anchor is a mirror image. On October 6, 2025, ETFs saw +$1.21 billion in inflows, which Santiment marked as a “sell signal at ATH”, inflows peaking exactly as price topped. Now the inverse: heavy outflows clustering near the lows, which they read as a strong fear signal. Their thesis is that the best buying opportunities have historically come when ETF investors and retail are most eager to exit.

Where Price Sits

Bitcoin trades around $60,185 at the time of writing, after reaching $61,050 and attempting to stabilize following the June decline that bottomed near $58,000. All three major moving averages sit well overhead as resistance, and momentum is recovering off the lows rather than reversing, a tentative steadying, not a confirmed turn.

The Tension Between the Two Reads

Both analysis frame the crowd’s exit constructively, but in ways that don’t fully fit together, and that’s worth being honest about. Darkfost reads it as structural institutionalization: retail replaced by institutions and ETFs. Santiment reads it as contrarian capitulation: weak hands leaving strengthens the bottom case. Both are reasonable, and both are interpretations, not confirmed outcomes.

The tension is real. If retail is structurally “extinct,” permanently migrated to ETFs as Darkfost suggests, then Santiment’s “they’ll capitulate and then return to buy” logic weakens, because you can’t get a retail-driven recovery from a cohort that has left for good. The two theses can’t both be fully true. Either retail comes back (supporting the contrarian bottom case) or it has structurally gone (supporting institutionalization), but not both.

What It Doesn’t Tell You

The critical limit is that none of this is predictive. Retail being absent doesn’t mean price bottoms; it can equally mean the market has lost a demand source that historically drove rallies. Santiment’s own framing is careful, outflows “can pressure price in the short term” even as they build the longer-term bottom case, so the contrarian signal is a probabilistic historical tendency, not a timing tool.

What both datasets confirm is the phenomenon, not the outcome: the retail and ETF crowd is exiting Bitcoin at historic intensity. Whether that clears the way for a bottom or removes a demand driver the market needs is exactly what the data can’t resolve. It describes who has left, not where price goes next.

This article is for informational purposes only and does not constitute financial advice. Consult a professional before making investment decisions.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP.

Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem.

To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem.

His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.

Be the first to comment