Peter Schiff posted on June 3 that Bitcoin has too much complacency to be near a bottom and predicted a fall below $20,000 after $50,000 breaks. The same week, Santiment confirmed crowd sentiment hit its most bearish reading in the entire measured period – which historically is not where complacency lives.

Key Takeaways

- Crowd sentiment hit -164 on June 3, its cycle low.

- 472 BTC obituaries. $100 each equals $66M today.

- The real selloff driver was $2.43B in May ETF outflows.

- Strategy net accumulated 170,000 BTC against 32 sold.

What Schiff Said

Peter Schiff posted two warnings on June 3. The first argued that Bitcoin’s complacency levels were incompatible with a genuine market bottom, predicting that a break below $50,000 would trigger a rapid collapse toward $20,000 and shake long-term holders into capitulation.

There is way too much complacency in Bitcoin for the market to be anywhere near a bottom. When Bitcoin breaks $50K, it should be a quick fall below $20K, which should be a big enough drop to shake the conviction of long-term HODLers, causing many to finally throw in the towel.

— Peter Schiff (@PeterSchiff) June 2, 2026

The second focused on Strategy’s preferred stock STRC, which had fallen to $94.85, putting its yield at 12.12%. Schiff’s argument was mechanical: the lower STRC falls, the higher Strategy must raise its dividend to bring the share price back toward $100, which means burning through cash faster and eventually forcing Bitcoin sales to fund the payments.

$STRC is down to $94.85, putting the current yield at 12.12%. The lower the price falls, the higher $MSTR will have to increase the dividend to bring the share price back up to $100. That means MSTR will run out of cash much sooner, pulling forward Bitcoin sales to fund payments.

— Peter Schiff (@PeterSchiff) June 3, 2026

Both arguments share the same underlying thesis: Bitcoin is fragile, Strategy is overextended, and the current selloff is the beginning of something much deeper.

That framing sets up a specific question worth examining: if the market is not complacent, what actually caused the drop, and is the explanation the market settled on accurate?

The 32 Bitcoin Problem

The market narrative that emerged in the days following Strategy’s SEC disclosure assigned significant blame for the selloff to the sale of 32 BTC, worth approximately $2.5 million. That sale triggered headlines, sentiment shifts, and contributed to a broader panic that, according to CoinGlass data, ultimately produced $1.61 billion in liquidations over 24 hours.

The arithmetic deserves scrutiny. Strategy manages 843,706 BTC. The 32 coins it sold represent 0.0038% of its holdings. In the same week, Strategy raised $128.3 million by selling its own equity, a transaction 50 times larger than the Bitcoin sale that received a fraction of the attention. A $2.5 million transaction in a market with a trillion-dollar asset class could mathematically be described as a rounding error.

The more structurally honest explanation is that the sale itself was never the point. The signal was. And the signal was deliberate. On Strategy’s Q1 earnings call, Saylor told investors he would “probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.” The framing was explicit: the sale was designed to demonstrate that Bitcoin could function as usable capital rather than an untouchable vault. Strategy’s philosophy has never been “never sell a single coin.” It has always been to be a net accumulator. Against the 32 coins sold, Strategy has accumulated over 170,000 BTC this year. Saylor measures himself on one number: Bitcoin per diluted share. By that metric, using 32 coins to defend the dividend was discipline, not distress.

One day after the sale disclosure, Saylor posted two words on X: “Back to Work.”

₿ack to Work pic.twitter.com/MmDLwySJpn

— Michael Saylor (@saylor) June 3, 2026

The post attracted 1.4 million views. Whether it signals that Strategy had already resumed accumulation is unverifiable from public data. But the timing and framing are consistent with someone who viewed the transaction as closed rather than consequential.

What Sentiment Actually Shows

The complacency argument does not only fail on the mechanics of the Strategy sale – it also fails on what the sentiment data recorded during the same period.

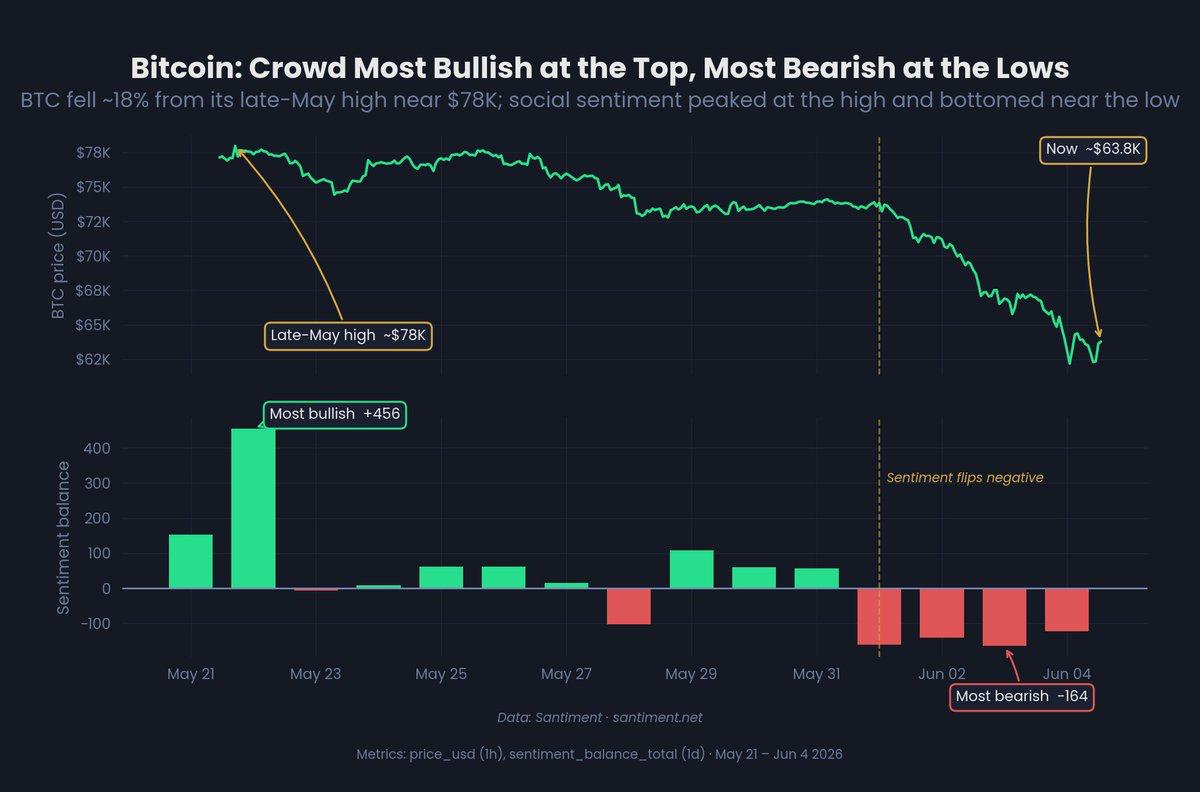

Santiment data confirms social sentiment on Bitcoin ran strongly positive at +456 on May 22, when price was near its late-May high around $78,000. As price declined, sentiment followed it lower, turning negative and bottoming at -164 on June 3 – the most bearish reading of the entire measured period – with Bitcoin near its lows around $63,500 at the time of writing.

The pattern Santiment identified is the inverse of complacency. The crowd was most bullish at the top and most bearish at the bottom, moving with price rather than ahead of it. That is textbook reactive sentiment, not the stubborn optimism that typically characterizes markets with genuine complacency problems. Peak bearishness at a potential local bottom is the inverse of where conviction usually pays. Schiff’s complacency claim requires the crowd to be dismissing the drop. The data shows the crowd is panicking into it.

The 472 Deaths of Bitcoin

Sentiment data addresses the crowd psychology argument. The historical record addresses something broader: whether the current moment is genuinely unprecedented or simply the latest in a long series of declared endings.

Bitcoin has been declared dead 472 times since its creation according to BitcoinDeaths. Each declaration marked a moment when the consensus view was that the asset was finished. A hypothetical investor who put $100 into Bitcoin at each of those 472 death declarations would hold $66,380,237 today.

The current moment has produced a fresh wave of obituaries. Bitcoin has dropped approximately 50% from its October 2025 cycle high of $126,000. Schiff’s prediction would represent an 84% peak-to-trough decline, according to BitcoinDeaths, matching the severity of the 2018 bear market. That is possible. It has happened before. But the 472 prior declarations of Bitcoin’s death share a common feature: they were all wrong. Not because Bitcoin is immune to decline, but because the asset has consistently found buyers at levels the consensus declared unsustainable.

The Real Drivers Are Not 32 Coins

History provides context, but the more immediate question is what actually produced this specific decline, and whether the explanation that dominated headlines holds up against the data.

The actual structural pressures behind the current decline are documented and measurable. SoSoValue data confirms US spot Bitcoin ETFs recorded $2.43 billion in net outflows in May 2026, the worst monthly reading of the year. Institutional capital has been rotating toward AI and semiconductor equities, which have produced significantly stronger returns in the same period. The Federal Reserve has shown no urgency to cut rates, keeping the cost of capital elevated and reducing the appetite for speculative risk assets.

These are the forces that produced the decline. The sale may have been the headline that crystallized the sentiment shift, but the underlying pressures were already in place. Schiff is correct that the selloff has real drivers. Where the argument breaks down is in treating the symptom, Saylor’s symbolic sale, as the cause, and in characterizing a market at its most bearish sentiment reading

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice. Coindoo.com does not endorse or recommend any specific investment strategy or cryptocurrency. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

Be the first to comment