The former chief risk officer of Silvergate revealed she made the decision to settle with the US securities regulator in 2024 to avoid a “multi-year battle” in court, where she was accused of misleading investors about anti-money laundering rules and how the bank monitored crypto customers.

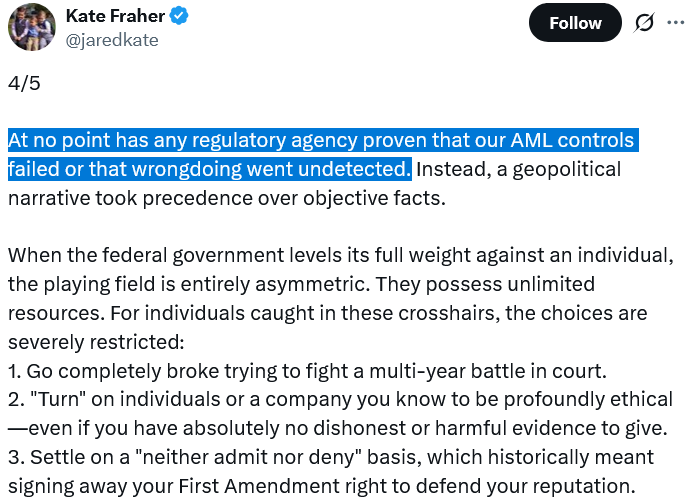

In her first public comments about her settlement with the SEC on Wednesday, Kate Fraher claimed that no financial agency proved that Silvergate’s anti-money laundering controls had failed, and that she only opted to settle to “move forward.”

Fraher had agreed to a civil penalty of $250,000 and was banned from serving as a company executive or board director for five years.

“The process itself is designed to apply maximum pressure, and the human costs are real. I was personally de-banked and had credit lines summarily closed—an aggressive tactic used to disrupt daily life and force compliance,” she said.

The comments provide more insight into the circumstances surrounding the wind-down of Silvergate, a crypto-friendly bank that voluntarily closed following the collapse of FTX. Fraher said her ability to comment came after the SEC rescinded the long-standing “gag rule” on Monday.

Source: Kate Fraher

Fraher said the wind-down was not because of a “bank run” or market volatility from FTX’s collapse in November 2022, even as the bank experienced a deposit run of around 70%.

Instead, Fraher said the company chose to wind down because the “broader administrative and regulatory pressure levied against the digital asset industry made operating a viable business impossible.”

Many crypto industry pundits labeled this as “Operation Chokepoint 2.0,” an unconfirmed plan in which US financial regulators cut off banking services to crypto companies in an attempt to restrict their ability to operate within the broader financial system.

Silvergate wasn’t the only crypto-friendly bank affected by the strict measures, which intensified following the collapse of FTX in November 2022.

Signature Bank and Silicon Valley Bank also shut down in early 2023, in part due to deposit runs, liquidity stress and contagion effects tied to FTX and several crypto lending platforms that went bankrupt in 2022.

Related: Trump-backed Truth Social pulls bids for crypto ETFs

But Fraher said by the beginning of 2023, it had weathered the FTX collapse by restructuring the business with “appropriate capital levels” and a “right-sized workforce” to continue operations safely.

Gag policy was unconstitutional, Fraher argues

Fraher applauded the current Paul Atkins-led SEC leadership for ending the gag rule, which she described as an “unconstitutional policy.”

“I am glad the right to speak the truth has finally been restored,” Fraher said, adding: “We must continue to talk about the long-term professional and personal toll exacted on individuals by regulation through enforcement.”

Magazine: 5 tech predictions the mainstream media got horribly wrong

Be the first to comment