Review Snapshot

| Category | Assessment |

|---|---|

| Company | Strategy Inc., formerly MicroStrategy |

| Ticker | MSTR |

| Core Identity | Bitcoin treasury company with enterprise analytics software |

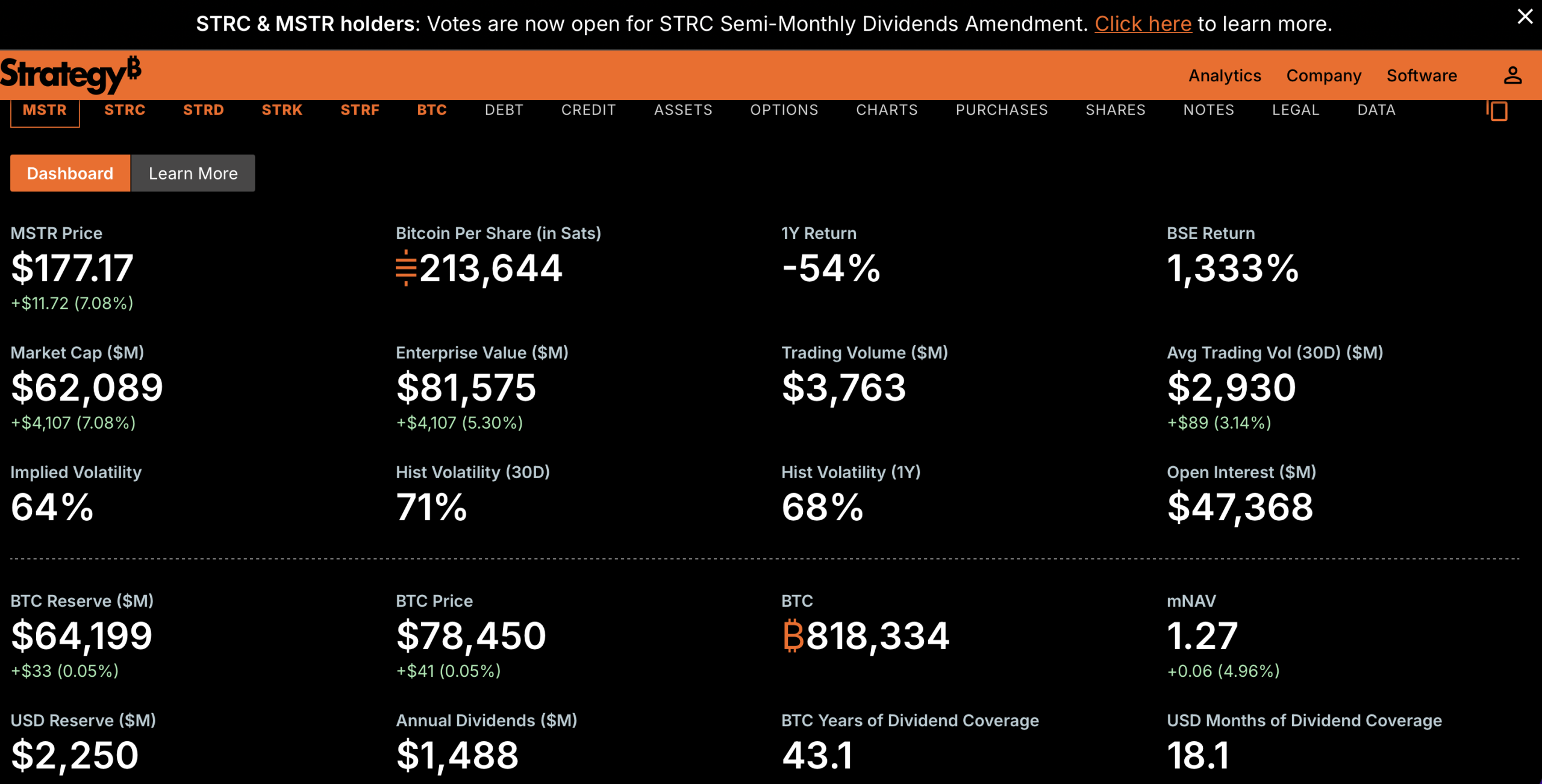

| Bitcoin Holdings | 818,334 BTC as of the latest public purchase dashboard |

| Average BTC Cost | $75,537 per BTC |

| Main Bull Case | Leveraged public equity exposure to Bitcoin accumulation |

| Main Bear Case | Capital-structure complexity, dilution risk, Bitcoin volatility, and premium compression |

| Risk Level | Very High |

| Editorial Score | 7.4/10 |

What Is Strategy?

Strategy is one of the most unusual public companies in the world. It began as MicroStrategy, a business intelligence software company, but now trades primarily as a Bitcoin treasury vehicle with an enterprise analytics business attached. Its investor profile is no longer driven only by software revenue, customer renewals, or enterprise AI adoption. It is driven by Bitcoin holdings, Bitcoin per share, financing access, market premiums, preferred stock demand, and the company’s ability to keep accumulating BTC without breaking the balance sheet.

The company defines itself as the first and largest Bitcoin Treasury Company. Its investor relations page frames the strategy around Bitcoin as the primary treasury reserve asset, funded through equity, debt, cash flow, and fixed-income style instruments. That makes MSTR different from a Bitcoin ETF. An ETF passively holds Bitcoin. Strategy actively issues securities, manages leverage, builds dollar reserves, maintains a software business, and tries to increase Bitcoin exposure per common share.

Bitcoin Holdings And Treasury Model

Strategy’s Bitcoin position is the whole review. The latest public Bitcoin purchases dashboard lists 818,334 BTC acquired at an average cost of $75,537 per BTC, for a total cost of about $61.814 billion. That makes Strategy the dominant public-company Bitcoin holder by a wide margin.

The model is simple in direction but complex in execution. Strategy raises capital, buys Bitcoin, holds it as a long-term reserve asset, and structures securities that give investors different forms of exposure. Common stock gives the most direct upside and downside to the full business. Preferred securities and credit-like instruments create different payout profiles, but they also add obligations, dilution paths, and refinancing pressure.

The key performance question is whether Strategy can keep increasing Bitcoin per share without destroying shareholder value through excessive issuance. Buying Bitcoin is easy when capital markets are open and the stock trades at a premium to the company’s Bitcoin net asset value. It becomes harder when Bitcoin falls, the premium narrows, preferred investors demand higher yields, or common shareholders resist dilution.

The Capital Stack

Strategy’s structure now includes common stock, several preferred securities, debt, and a large Bitcoin reserve. That capital stack is the engine behind the strategy. It lets the company raise money in different markets instead of relying only on common equity sales.

The preferred stock layer is especially important in 2026. Strategy’s STRC information makes clear that preferred securities such as STRF, STRC, STRE, STRK, and STRD are not collateralized by Bitcoin holdings and only have a preferred claim on residual company assets. That detail matters because investors sometimes assume every Strategy security is a direct claim on Bitcoin. It is not.

This structure creates amplification. If Bitcoin rises and capital markets stay open, Strategy can issue securities, buy more BTC, and potentially increase Bitcoin per share. If Bitcoin falls for long enough, the same structure can create stress through preferred dividends, interest obligations, fair-value losses, lower equity demand, and weaker investor confidence.

Software Business Review

Strategy still has an enterprise software business, and it should not be ignored. The company’s Strategy One platform combines business intelligence, a governed semantic layer, self-service analytics, and AI-powered workflows for enterprise users. Its Mosaic product positions the company around governed data definitions and AI-ready enterprise analytics.

The software division gives Strategy operating substance beyond Bitcoin custody. It contributes customer relationships, brand history, product infrastructure, and cash flow potential. However, the market no longer values Strategy mainly like a software company. The analytics business matters as a cash-flow and credibility layer, but MSTR trades as a Bitcoin-linked equity with software optionality rather than a classic enterprise software stock.

That is both a strength and a limitation. The software business can support operations and give Strategy a real company base. It cannot fully offset Bitcoin volatility when the balance sheet is dominated by BTC.

Why Bitcoin Investors Watch MSTR

MSTR gives investors something different from spot Bitcoin. It offers leveraged Bitcoin exposure through a public equity wrapper. When Bitcoin rises and Strategy’s market premium expands, MSTR can outperform Bitcoin. When Bitcoin falls, funding conditions tighten, or the premium compresses, MSTR can fall harder than Bitcoin.

That makes MSTR a reflexive vehicle. A rising stock price can make capital raises easier, which can fund more Bitcoin purchases, which can increase market attention, which can support the stock. The loop can work in reverse when Bitcoin weakens. Lower share prices reduce issuance efficiency, premium compression reduces the value of new equity sales, and preferred or credit obligations become more visible.

For Bitcoin believers, Strategy is a high-conviction treasury machine. For skeptics, it is a financial structure that depends too heavily on Bitcoin price, capital-market access, and continued investor appetite for MSTR-linked securities.

Strengths

Strategy’s biggest strength is scale. Holding more than 818,000 BTC gives the company unmatched corporate Bitcoin exposure and makes it a central institution in the Bitcoin capital markets narrative.

The second strength is capital-market creativity. Strategy has built a menu of securities around Bitcoin exposure, including common equity and preferred instruments. That gives it more funding flexibility than a normal operating company.

The third strength is narrative clarity. Investors know what MSTR is. It is the public-company Bitcoin treasury trade. That clarity can attract capital when Bitcoin momentum improves.

The fourth strength is operational history. Strategy has survived several Bitcoin drawdowns, continued accumulating, maintained a software business, and kept the treasury strategy visible through detailed purchase disclosures.

Weaknesses And Risks

The biggest risk is Bitcoin concentration. Strategy is not diversified in any meaningful treasury sense. If Bitcoin suffers a deep bear market, MSTR absorbs that through asset value, earnings volatility, stock performance, investor confidence, and financing flexibility.

The second risk is dilution. Strategy can create value when it issues stock above Bitcoin net asset value and uses proceeds to buy more BTC. The same mechanism becomes less attractive when the premium narrows or disappears.

The third risk is fixed obligations. Preferred dividends, debt service, and refinancing needs matter more when Bitcoin weakens. Strategy does not need to sell Bitcoin immediately in every downturn, but the capital stack adds pressure that a simple spot Bitcoin holder does not face.

The fourth risk is premium compression. If investors can buy spot Bitcoin ETFs, Bitcoin miners, or other treasury companies more efficiently, MSTR’s premium can shrink. A lower premium changes the math of future Bitcoin accumulation.

Verdict

Strategy is one of the most powerful Bitcoin proxy investments, but it is not a simple Bitcoin substitute. It is a leveraged, capital-market-driven treasury company with a real software business, massive BTC holdings, and a complex securities stack built around long-term Bitcoin accumulation.

The bull case is compelling when Bitcoin is rising, MSTR trades at a premium, capital markets stay open, and Bitcoin per share grows. The bear case is equally serious when Bitcoin falls, preferred obligations become more expensive, equity issuance becomes less attractive, and investors question whether the premium is still justified.

Strategy earns a 7.4/10 because it has unmatched Bitcoin scale, clear strategic identity, financial creativity, and real operating infrastructure. It does not score higher because MSTR carries very high volatility, dilution risk, capital-structure complexity, and extreme dependence on Bitcoin’s long-term price path.

Conclusion

Strategy is best understood as the institutional Bitcoin treasury trade in public equity form. It is not only a software company, not only a Bitcoin holder, and not only a leveraged stock. It is a financial vehicle designed to accumulate Bitcoin, issue securities around that exposure, and make Bitcoin per share the central long-term metric.

For investors bullish on Bitcoin, Strategy can offer amplified upside and a unique capital-market structure. For risk-controlled investors, it can be too volatile, too concentrated, and too dependent on market premiums. The strongest case for MSTR is that Bitcoin becomes more valuable over time and Strategy keeps accumulating efficiently. The biggest risk is that Bitcoin weakness, dilution, and capital-stack pressure turn that same engine against shareholders.

Be the first to comment