Fundstrat’s Tom Lee thinks crypto’s weakness is a price problem, not a broken thesis. Speaking with Anthony Scaramucci on SALT, he laid out a wide-ranging bull case.

Key Takeaways

- Tom Lee argues crypto isn’t losing to AI, it’s a downstream beneficiary of it.

- He frames the August-to-October window as where long-term investors look to enter.

- His Ethereum and BitMine views come with a direct commercial interest attached.

- He reads today’s extreme negative sentiment as historically a good sign.

On the SALT channel hosted by SkyBridge Capital’s Anthony Scaramucci, Fundstrat’s Tom Lee made a wide-ranging case for why he thinks crypto’s current weakness is a price problem, not a fundamentals problem. Across roughly 20 minutes, the two covered AI, the four-year cycle, Ethereum, quantum risk, Michael Saylor’s Strategy, and the grim state of market sentiment. Lee is also chairman of the Ethereum treasury company BitMine Immersion Technologies, and that’s worth keeping in mind, because several of his arguments line up with positions his company holds.

Crypto as AI’s Downstream, Not Its Casualty

Scaramucci opened with the question on everyone’s mind: is AI sucking capital out of crypto? Lee acknowledged that AI is capturing incremental investment dollars on the margin, but he rejected the idea that this breaks the crypto thesis. His framing is that crypto isn’t competing with AI, it’s downstream of it. As Wall Street upgrades what Lee called its outdated tech stack onto crypto rails, the structural story keeps compounding even while price lags. “Crypto is still a really important downstream story to AI,” Lee said. In his view, the near-term price action and the long-term fundamental story are simply on different clocks, looking two years out, he sees a future that’s still very crypto-centric.

Why Ten Days a Year Decide Everything

Asked whether Bitcoin is still running on a four-year cycle, Lee validated the framework, but as a tool for longer-term, tactical investors rather than a universal timing device. His supporting argument comes down to how concentrated Bitcoin’s gains really are:

- The 10-day rule: Bitcoin makes most of its annual gains in about 10 days. Exclude the 10 best days each year, Lee says, and Bitcoin’s return flips to roughly -27% annually.

- It’s not unique to crypto: missing the 10 best days in the S&P since 1929 turns a 9% annual compound return negative.

- The effect is growing: over the last three years, that gap has been worth more than 24 percentage points.

The practical takeaway Lee draws is about timing windows. The early part of the four-year cycle, roughly August to October, is when he thinks longer-term investors begin considering entry, potentially with prices in the $50,000 to $60,000 range. He frames this as especially relevant for people new to crypto who are used to quarterly earnings catalysts, because crypto has no equivalent announcement structure and no centralized entity making disclosures. “The best investment decisions really have required people to have a longer time frame,” Lee said.

The way Lee connects these pieces, from today’s sentiment through to the long horizon he says success demands, follows a clear sequence:

Current Market Sentiment

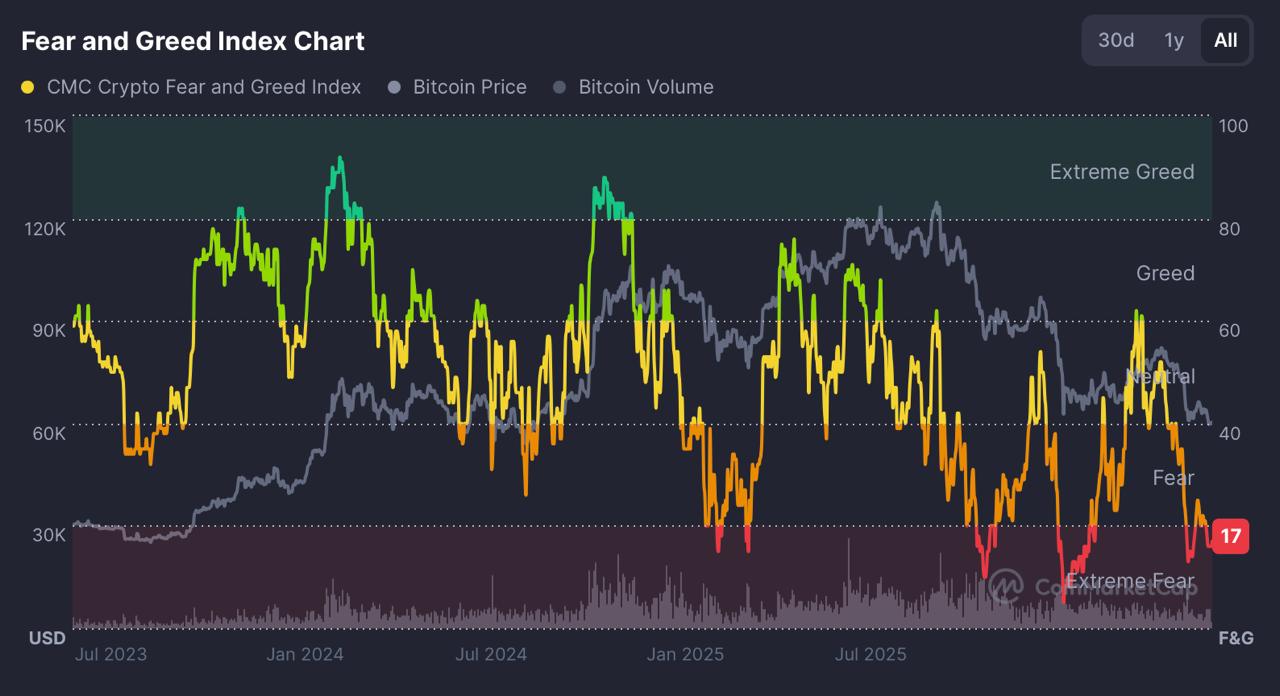

Sentiment is at extreme lows; historically, this level of pessimism has often preceded recoveries.

August – October Window

Target period for long-term investors to consider entries, with potential price points between $50,000 and $60,000.

Long-Term Fundamentals

Crypto acts as a “downstream beneficiary” of AI, providing necessary infrastructure for human sovereignty and decentralized identity.

Cyclical Horizon

Success requires a long time frame, as Bitcoin gains are historically concentrated in just 10 days per year.

The Ethereum Thesis He Has a Stake In

Scaramucci put a pointed scenario to Lee: imagine an $8 million BitMine position now worth around $3 million, what’s the message? Lee didn’t pretend that’s the outcome anyone wanted, but pivoted to fundamentals. This is where his BitMine interest is most relevant, since the company is an Ethereum treasury vehicle, so his bullishness aligns with his commercial position, and readers should weigh it accordingly. His Ethereum thesis rests on three concrete developments:

- Tokenization: more real-world assets are being tokenized on Ethereum, and most major funds and stocks being tokenized choose it because it’s the most widely used blockchain.

- Quantum resistance: the Ethereum Foundation is upgrading the protocol to be quantum-proof.

- Privacy: new privacy features are being added.

“Ethereum has gained additional assets. More real-world assets are being tokenized on Ethereum,” Lee said. The forward-looking part of his case ties Ethereum to AI: he argues AI engineers are realizing that downstream of the AI story sits a need to prove identity and decentralized control, and that centralized AI systems risk what he calls a “Skynet” scenario. Decentralized blockchains, Ethereum specifically in his telling, become the infrastructure that protects human sovereignty as AI grows more powerful. He frames this as an engineering recognition already happening inside the AI community, though it remains his interpretation of where things are heading.

When the Agents Get Richer Than the Humans

Lee pushed that idea to a provocative conclusion. Before long, he argued, AI agents will be producing income as our delegated entities, earning and accumulating wealth, and could eventually hold more than we do. “AI agents might actually become wealthier than us,” Lee said, to the point where we start asking whether we work for them or they work for us. The question that follows, in his framing, is whether the systems managing that wealth are centralized or decentralized, which is exactly what he believes makes decentralized blockchains relevant to the AI economy, not just the crypto economy.

The Quantum Problem Hiding in Old Wallets

Scaramucci 9:46 whether Lee was worried about the quantum threat to Bitcoin specifically. Lee separated the two ecosystems. Bitcoin’s challenge, he said, isn’t whether it can become quantum-resistant (it can), but how to handle legacy wallets, by some estimates as much as a third of all Bitcoin sits in older wallets that would need upgrading. He laid out the options the community is weighing:

- Forking the chain.

- Burning Satoshi’s coins.

- Whitelisting or protecting coins, so that if a quantum system started draining legacy wallets, say 50 Bitcoin at a time, those coins could be made impossible to spend.

“It really has to do with how to handle the number of legacy wallets,” Lee said. He admitted he doesn’t know the answer but voiced faith the Bitcoin community will solve it. Ethereum, he added, has a somewhat easier path, since both its protocol and its wallets can be upgraded, and smart-contract platforms are using formal verification to make their code resistant to exploits.

Saylor, Short Sellers, and the B-17 Analogy

Scaramucci then raised Michael Saylor, describing him as being in the crosshairs of short sellers trying to crack his capital structure and flush him out of the 900,000-plus Bitcoin his company holds, and asked how, or whether, he could get out of it. Lee reached for a military analogy: a formation of B-17 bombers over Germany, where the plane that falls behind is the one the fighters pick off. Strategy’s public capital structure, he noted, is visible and testable by public markets in a way the Bitcoin blockchain itself is not, so that’s the structure being tested.

Lee’s prescribed defense was specific, and it’s his strategic read rather than a recommendation: raise cash and build the equity cushion, but don’t sell Bitcoin. His reasoning is that Saylor functions effectively as a central bank of Bitcoin, so a sale from him spooks the market disproportionately, a point Scaramucci agreed with directly. The route Lee said he would favor, while adding “I’m not Michael Saylor,” is raising cash by selling MSTR common stock, which thickens the equity cushion without sending a Bitcoin-sale signal. The priority, in his words, is “raising cash without selling Bitcoin,” because when Saylor sells, “it creates a spooking.”

The One Question That Breaks the BitMine Bull Case

Scaramucci, who disclosed that he personally owns BitMine, laid out the bull case for the company Lee chairs: the largest ETH treasury vehicle, producing staking yield in a flywheel that adds to its Ethereum stack, institutionally accessible, with an investment in Mr. Beast he considers undervalued. Then he asked the sharper question, what would make Lee a BitMine bear? In answering, Lee first detailed the company’s deliberately conservative footing:

- A large cash position of about $600 million.

- Roughly 80% of its Ethereum staked, generating over $250 million a year in staking rewards.

- Several hundred million dollars in annual free cash flow.

- Disclosed investments including Mr. Beast and 8Co, plus close work with Ethereum Foundation spinoffs such as ETH Labs.

Then came the candid part. Lee reduced the entire bear case to a single condition: the thesis fails if decentralized infrastructure turns out to be unnecessary. “If we’re comfortable relying on Skynet and Visa to control our future, then we don’t need decentralized blockchains,” Lee said. He framed this not as a price call but as a foundational question about whether decentralized blockchains have a future role at all, a notably honest way to state the risk, even if it’s cast in his own terms.

What 17 Years of Wireless Stocks Taught Him

Scaramucci recalled their post-FTX conversation, when Lee held conviction and Bitcoin later ran from $15,000 to $126,000 (now back near $58,000-$59,000), and asked about his cool-headedness through drawdowns.

Lee grounded his patience in the first 17 years of his 35-year career, covering wireless stocks. Subscriber growth ran a reliable 40% a year and the innovation was parabolic, yet the stocks were violently cyclical, partly because the public dismissed wireless as a “yuppie toy” and didn’t see the value it was capturing. He watched those stocks make huge moves and suffer huge drawdowns while the fundamentals kept compounding.

He invoked the Japanese word kiki, crisis, built from two characters meaning danger and opportunity, arguing that instinct pushes people toward the danger reading while history rewards the opportunity one. He pointed to a familiar list of slow-then-sudden movers:

- NVIDIA, range-bound for years before its parabolic move.

- Memory stocks, flat for about two years before they exploded.

- JPMorgan, stuck around $17 for roughly 13 of 15 years before clearing $200.

“In every drawdown, you have to focus on the opportunities,” Lee said.

“Dark Days, but July Is a New Month”

To close, both men turned to the mood in the market, and it was bleak. Scaramucci ran through the indicators he’d been seeing, people indifferent about Bitcoin and Ethereum at events, Google searches down, the RSI at an all-time low, and a fear and greed index worse than after the FTX collapse, the kind of backdrop, he noted, that’s usually a good time to be buying.

Lee agreed and added the longer view from 35 years on Wall Street: sentiment this bad has generally been a constructive sign. “Sentiment is as bad as it can get right now. Which, generally, when sentiment has been this bad, that’s usually been a good sign,” Lee said. He allowed that some of the late-June selling might be quarter-end window dressing, then landed on a simpler note: “July is a new month.”

Reading Lee’s Case With Clear Eyes

Lee’s throughline is consistent: fundamentals compound, price doesn’t follow in real time, and drawdowns are where opportunity concentrates. It’s a coherent, experienced framework, and his sentiment and four-year-cycle observations rest on real historical patterns. The caveats matter just as much. Several of his strongest convictions, on Ethereum and BitMine especially, align directly with positions his company holds, and Scaramucci disclosed his own BitMine stake too, so the bullishness carries a commercial interest a neutral observer wouldn’t have.

The AI-and-decentralization arguments are forward-looking theses, not established facts. And the idea that bad sentiment makes for a good buying moment is a probabilistic historical observation, not a guarantee, sentiment can stay bad, and the worst readings don’t always mark the bottom. The framework is worth understanding; the conclusions are theirs, and several come with a stake attached.

This article is for informational purposes only and does not constitute financial advice. Consult a professional before making investment decisions.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP.

Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem.

To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem.

His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.

Be the first to comment