Bitcoin’s ratio to gold has fallen further below its long-term trend than at any point since 2010. The oscillator tracking that gap printed minus 1.81 standard deviations this week, a deeper reading than either the 2015 or 2022 bear market lows.

Bitcoin has reached its most oversold level against gold on record, while prediction-market traders assign it only a 13% chance of outperforming gold and the S&P 500 in 2026. The divergence supports two competing interpretations: Bitcoin is trading at a rare relative discount, or investors no longer classify it as a monetary hedge.

Key Takeaways

- The BTC/gold oscillator has reached its most oversold reading on record.

- The only comparable historical signal preceded a roughly 660% Bitcoin rally, although the sample consists of a single prior event.

- Polymarket traders give Bitcoin a 13% chance of beating gold and the S&P 500 in 2026.

- The signal depends on whether investors still consider Bitcoin and gold comparable monetary assets.

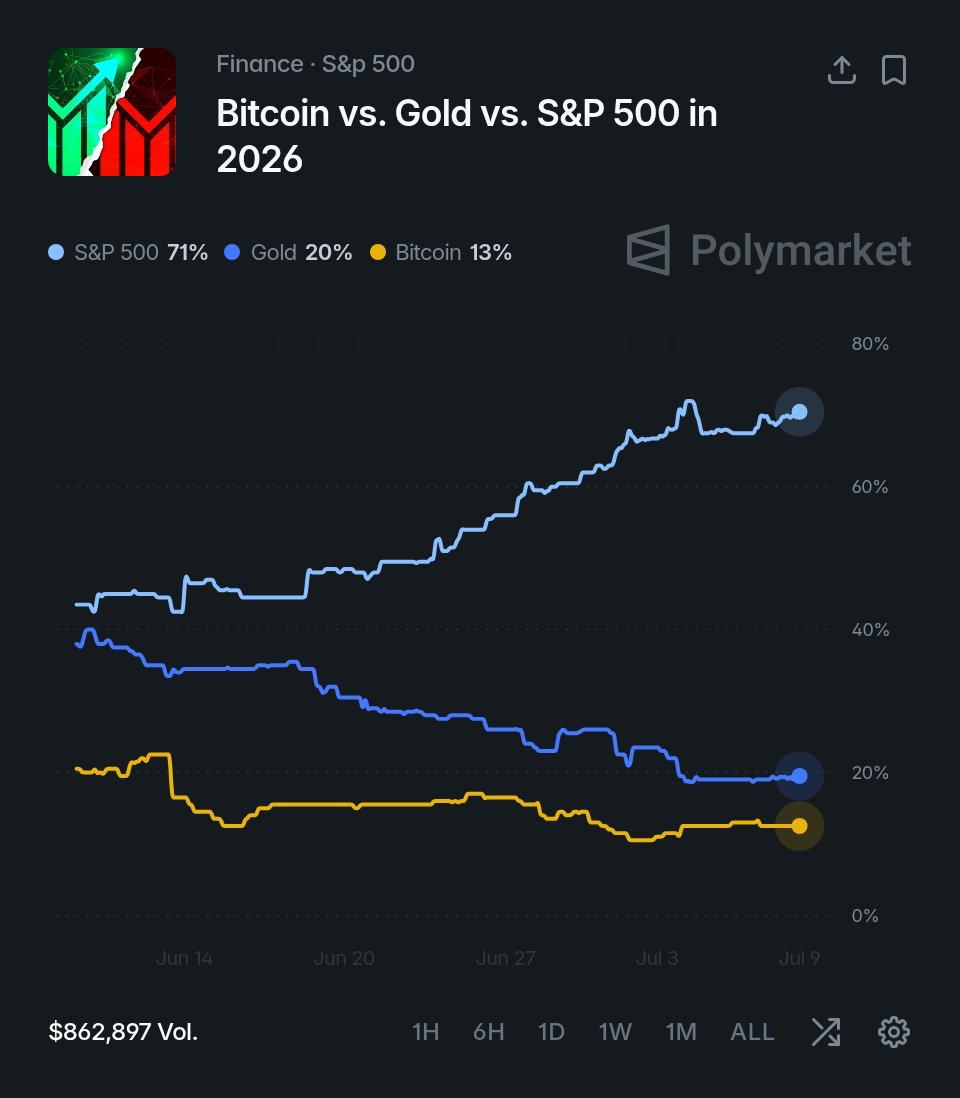

Prediction Markets Price Bitcoin as the Laggard

Polymarket traders wagering on the best-performing asset of 2026 currently assign the S&P 500 a 71% chance, gold 20%, and Bitcoin 13%. Bitcoin’s odds have declined from approximately 20% in mid-June, while the S&P 500 has risen from the mid-40% range.

The shift shows that traders willing to commit capital have become more confident that Bitcoin will finish behind both traditional assets, rather than merely reflecting its recent underperformance.

Prediction-market prices measure the positioning of participants on a specific platform, not the objective probability of an investment outcome. Liquidity concentration, large individual wagers, and changing sentiment can move the displayed odds without altering the underlying fundamentals of the assets.

The 13% reading therefore confirms weak expectations among Polymarket traders, but it cannot establish that Bitcoin will underperform over the full year.

The Mean-Reversion Case Has One Historical Precedent

The contrarian argument begins with the BTC/gold oscillator. The indicator has fallen to its most oversold reading in the available series, while the monthly chart is at its second-deepest oversold level.

According to a post from Cointelegraph, the only comparable signal preceded a Bitcoin rally of nearly 660% over the following years.

🔥 BULLISH: Bitcoin has reached its most oversold level against gold on record, a signal that last preceded a nearly 660% rally. pic.twitter.com/dnLuDgXdVF

— Cointelegraph (@Cointelegraph) July 10, 2026

An extreme deviation can support a mean-reversion trade because continued movement in the same direction requires the valuation gap to widen further. Bitcoin’s record relative weakness and its 13% prediction-market odds create that type of contrarian setup.

The historical comparison remains limited. A single previous occurrence cannot establish a repeatable relationship, particularly when the earlier rally developed under different liquidity, adoption, and macroeconomic conditions.

Cathie Wood presented the bullish interpretation this week using ARK’s Bitcoin-to-gold chart. She noted that the ratio remains above its previous two major lows despite Bitcoin’s weakness and gold’s simultaneous advance.

ARK expects the reversal to come from both sides of the pair: “we expect Bitcoin to gold to turn around,” Wood said, with Bitcoin rising as gold declines.

The forecast is consistent with ARK’s broader view of Bitcoin as the foundation of an emerging global monetary system. That long-term positioning is relevant when assessing the call because the firm is structurally exposed to the outcome it expects.

Recent positioning data provides additional context. As covered in recent cycle analysis, capital rotated from Bitcoin ETFs into the artificial-intelligence trade during the spring, approximately half of Bitcoin holders are underwater, and sentiment indicators have fallen to yearly lows.

Those conditions are consistent with capitulation, but they do not distinguish between a temporary valuation extreme and a longer-term loss of relative demand.

Schiff Challenges the BTC-to-Gold Comparison

Peter Schiff rejects the premise behind the oscillator rather than disputing the level itself. He argued this week that Bitcoin was never meaningfully correlated with gold despite its digital-gold branding.

Schiff instead pointed to Bitcoin’s former relationship with the Nasdaq, claiming that the correlation has weakened asymmetrically. Bitcoin no longer participates consistently when technology stocks rise, he wrote, “but I think it will still fall when the NASDAQ falls.”

Bitcoin was never really correlated to gold, despite the false claims that it’s digital gold. However, there was a strong correlation to the NASDAQ that has since broken down. Bitcoin no longer rises when the NASDAQ rises. But, I think it will still fall when the NASDAQ falls.

— Peter Schiff (@PeterSchiff) July 9, 2026

The bear case does not require the oscillator to be calculated incorrectly. It argues that mean reversion becomes less reliable when the assets in the ratio no longer occupy the same investment category.

If institutional portfolios increasingly treat gold as a monetary hedge and Bitcoin as a high-beta risk asset, the valuation gap can remain wide or expand further. Under that interpretation, the previous 660% rally offers limited guidance because it occurred while Bitcoin was still being adopted as an emerging monetary asset.

The Ratio Is Testing Bitcoin’s Market Classification

The three positions are based on different assumptions rather than different readings of the same price.

Polymarket traders are pricing Bitcoin as the likely laggard. ARK views it as a temporarily suppressed monetary asset. Schiff argues that comparing it with gold is no longer analytically useful.

At minus 1.81 sigma, the BTC/gold ratio cannot determine which classification is correct. A sustained recovery would support the argument that Bitcoin was temporarily mispriced during a macroeconomic and AI-driven capital rotation.

Further deterioration would indicate that investors are no longer willing to value Bitcoin alongside gold solely because both assets are scarce and independent of government issuance.

Bitcoin’s digital-gold thesis has not been disproved by one relative-value extreme. The market is nevertheless demanding evidence in the form of renewed strength against gold rather than accepting the classification through narrative alone.

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency markets are volatile and involve substantial risk. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP.

Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem.

To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem.

His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.

Be the first to comment