As late-stage funding swells despite fewer deals, crypto’s fundraising model is fundamentally changing. Data shows institutional “project finance” is now superseding traditional, retail-focused venture capital cycles.

Key Takeaways

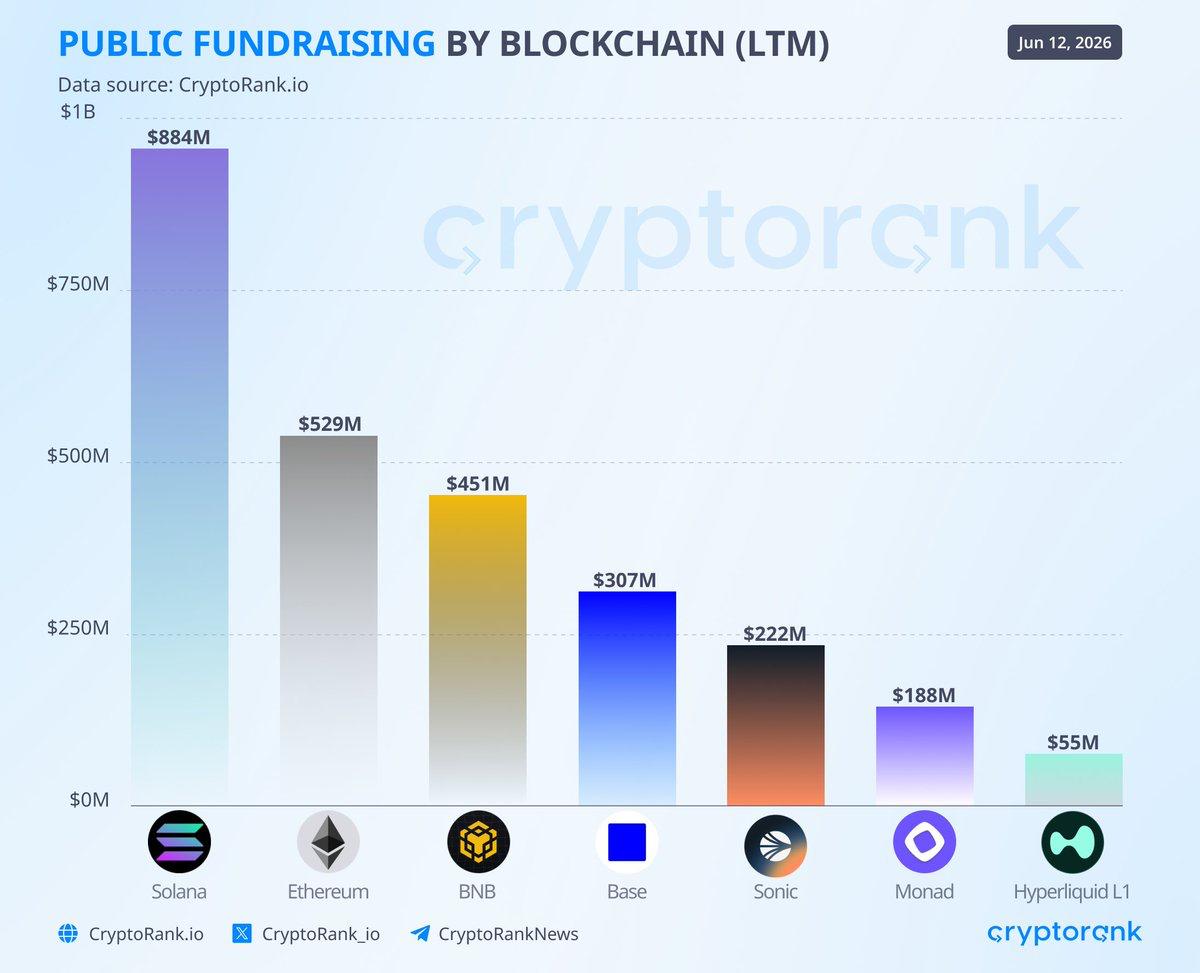

- Solana ecosystem leads 12-month public fundraising with $884M, ahead of Ethereum’s $529M.

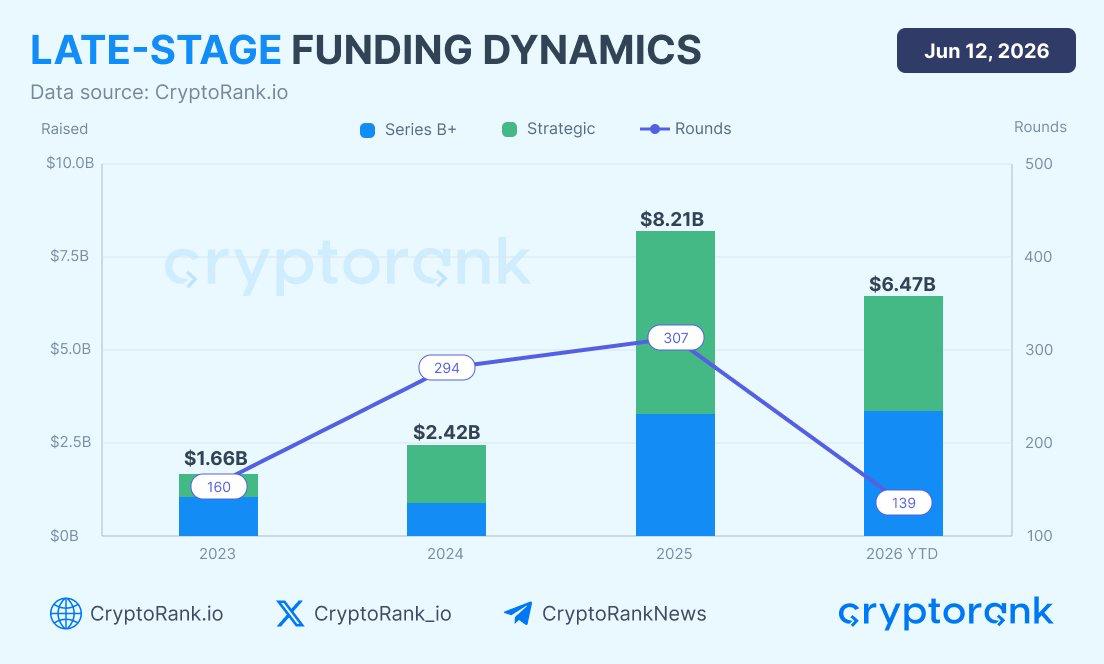

- Series B+ and Strategic funding grew from $1.66B in 2023 to $6.47B in 2026 YTD.

- 2026’s $6.47B arrived across just 139 rounds, versus 307 rounds in all of 2025.

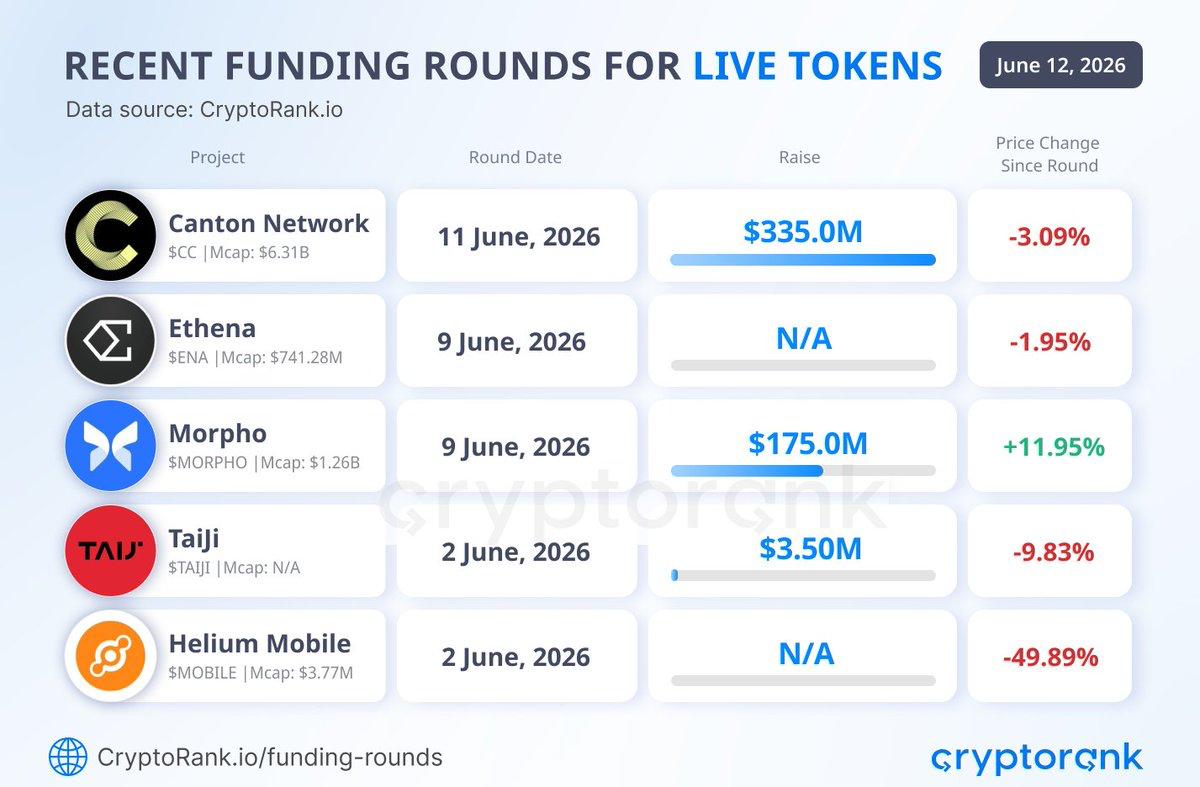

- Four of five recently funded live tokens trade below their round-date price.

Crypto fundraising in 2026 is consolidating around fewer winners taking larger checks. Three datasets published by analytics platform CryptoRank on June 12 sketch the same picture from different angles: public capital concentrating in three ecosystems, late-stage rounds growing while their count collapses, and token markets refusing to reward funding announcements on contact.

Solana Tops Public Fundraising, and Three Chains Take Most of It

According to CryptoRank data covering the last twelve months, the Solana ecosystem raised $884 million in public fundraising, the most of any blockchain, followed by Ethereum at $529 million and BNB Chain at $451 million. Base raised $307 million, Sonic $222 million, Monad $188 million, and Hyperliquid $55 million.

The distribution matters more than the ranking. The top three ecosystems account for roughly 71% of the capital across the seven chains tracked, a concentration CryptoRank attributes to public market investors favoring ecosystems with strong developer activity, active user bases, and clear narratives. Solana’s lead also lands in a week when its infrastructure argument received unusual mainstream exposure: tokenized SpaceX shares went live on the network the same day the company listed on Nasdaq.

Funding After the Token: Canton’s $355M Leads the Pack

“Funding doesn’t stop after token launch,” CryptoRank wrote on X, highlighting five projects with live tokens that announced new rounds over the past two weeks. The largest belongs to Canton Network: developer Digital Asset announced a $355 million round on June 11 led by a16z crypto, with a participant list that reads like a capital markets directory: ABN Amro, Apollo Funds, BNP Paribas, Citadel Securities, CME Ventures, Coinbase Ventures, HSBC, Polychain, S&P Global, SBI Group, SoFi, Tradeweb, and the Abu Dhabi Investment Authority among them. Morpho, the DeFi lending protocol, raised $175 million on June 9, while BNB Chain project Taiji added $3.5 million; Ethena and Helium Mobile disclosed rounds without amounts.

This strategic alignment is not theoretical, and the investor list doubles as a user list. BNP Paribas operates Neobonds, its asset tokenization platform, on Canton’s framework and issued the first Eurozone sovereign digital bond, a 30 million euro instrument for the Republic of Slovenia. Goldman Sachs built its GS DAP tokenization platform on the same Daml smart contract infrastructure, which hosted the European Investment Bank’s 100 million euro digitally native bond.

Visa joined Canton as a Super Validator in March and folded the network into its stablecoin settlement pilot. These institutions are not buying an asset to flip to retail; they are capitalization-anchoring the rails of their own next-generation bond, collateral, and settlement infrastructure.

The market’s verdict on these raises is the detail worth keeping. Per CryptoRank’s tracking, four of the five tokens trade below the levels they held on their round dates, with only Morpho gaining since its announcement. Fresh capital on the balance sheet no longer translates into token demand by default, and in Canton’s case, a raise that strengthens the company behind the network did little for the asset that trades on it.

Late-Stage Capital: Four Times the Money, Half the Rounds

The structural shift sits in CryptoRank’s late-stage data. Annual Series B+ and Strategic funding has grown from $1.66 billion in 2023 to $2.42 billion in 2024, $8.21 billion in 2025, and $6.47 billion in 2026 year to date, nearly a fourfold increase in deployed capital with half a year still to run.

Round count tells the opposite story: 160 rounds in 2023, 294 in 2024, 307 in 2025, and just 139 so far in 2026. Run the division and the average late-stage check has jumped from roughly $27 million in 2025 to about $47 million in 2026, more than four times the 2023 average. Capital is not spreading across the industry; it is stacking into fewer, larger bets.

Why Venture Is Losing to Project Finance

The mechanics behind the shift are worth spelling out. The classic crypto venture model depends on speed to liquidity: a fund invests in a private round, the project launches a token within a year or two, and retail demand at listing provides the exit that returns capital to limited partners. That machine requires retail to show up. CryptoRank’s post-round price data shows retail is no longer showing up, and when funding announcements stop producing rallies, the entire exit math of narrative-driven venture stops working.

Strategic investors run on different economics entirely. A bank or exchange writing a check into settlement infrastructure is not underwriting a token’s 30-day performance; it is underwriting cost reduction in clearing, collateral mobility, and cross-border asset movement over a five-to-ten-year horizon. Token price between here and there is nearly irrelevant to the thesis. CryptoRank notes that Strategic rounds now account for the majority of late-stage capital, and the Canton round is the template: nearly every name on its investor list is a future customer or counterparty of the network, not a passive allocator hunting an exit.

“Institutions need infrastructure that reflects how they actually operate,” Digital Asset CEO Yuval Rooz said of the raise, pointing to privacy, compliance, scale, and interoperability as the requirements for capital markets to move onchain, a framing in which the investors are the institutions he is describing.

| Dimension | Historic Venture Model (2021–2024) | Maturing Project Finance Model (2025–2026) |

|---|---|---|

| Primary capital source | Crypto-native VCs and retail speculators | Corporate treasuries, commercial banks, syndicates |

| Ecosystem preference | Narrative-heavy, speculative testnets | Proven developer density and active user footprints |

| Success metric | High-multiple token generation events | Operational integration, throughput, utility stability |

| Token reaction to funding news | Hype-driven rallies on announcements | Subdued or flat; focus shifts to balance sheet viability |

What the Three Charts Say Together

Read as one dataset, the pattern resembles a maturing industry more than a bull market. Public raises concentrate in ecosystems with demonstrated usage, late-stage capital flows through fewer and larger strategic checks from institutions with operational intent, and token prices have stopped treating funding news as a buy signal. For projects, the bar has moved: a raise now proves survivability to investors, not upside to traders.

The numbers to watch from here are the 2026 round count, which would need a dramatic second-half acceleration just to match 2025’s 307, and whether Strategic capital’s majority share holds. If both trends persist, crypto’s funding market will end the year looking less like venture and more like project finance, with the winners chosen by the institutions that plan to use them.

The Operational Takeaway for Founders and Allocators

For founders, the data reframes the pitch. Strategic capital is buying B2B efficiency and integration, not explosive token upside, so projects positioned as infrastructure with named institutional use cases are raising at four times the average check size of two years ago, while narrative-first projects compete for a shrinking pool of classic venture rounds.

For liquid token investors, the post-round price table is the lesson: a funding announcement, even one with a16z and HSBC attached, has stopped functioning as a reliable buy signal. The metrics that separated Morpho, the only gainer in CryptoRank’s set, from the rest are organic fee generation and sustained usage, which suggests tracking revenue and developer retention now carries more signal than tracking raises.

This article is for informational purposes only and does not constitute financial advice. Consult a professional before making investment decisions.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP.

Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem.

To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem.

His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.

Be the first to comment