Strategy may tap its massive Bitcoin stack to fund dividends and obligations and continuously increase its holdings, Executive Chairman Michael Saylor said during the company’s earnings call on May 5.

Tune into @Strategy‘s Q1 Earnings Call live now on X. We’ll cover:

-Q1 financial results

-Digital Credit $STRC

-Digital Equity $MSTRFollowed by a live Q&A!https://t.co/j4rKKAvU0A

— Strategy (@Strategy) May 5, 2026

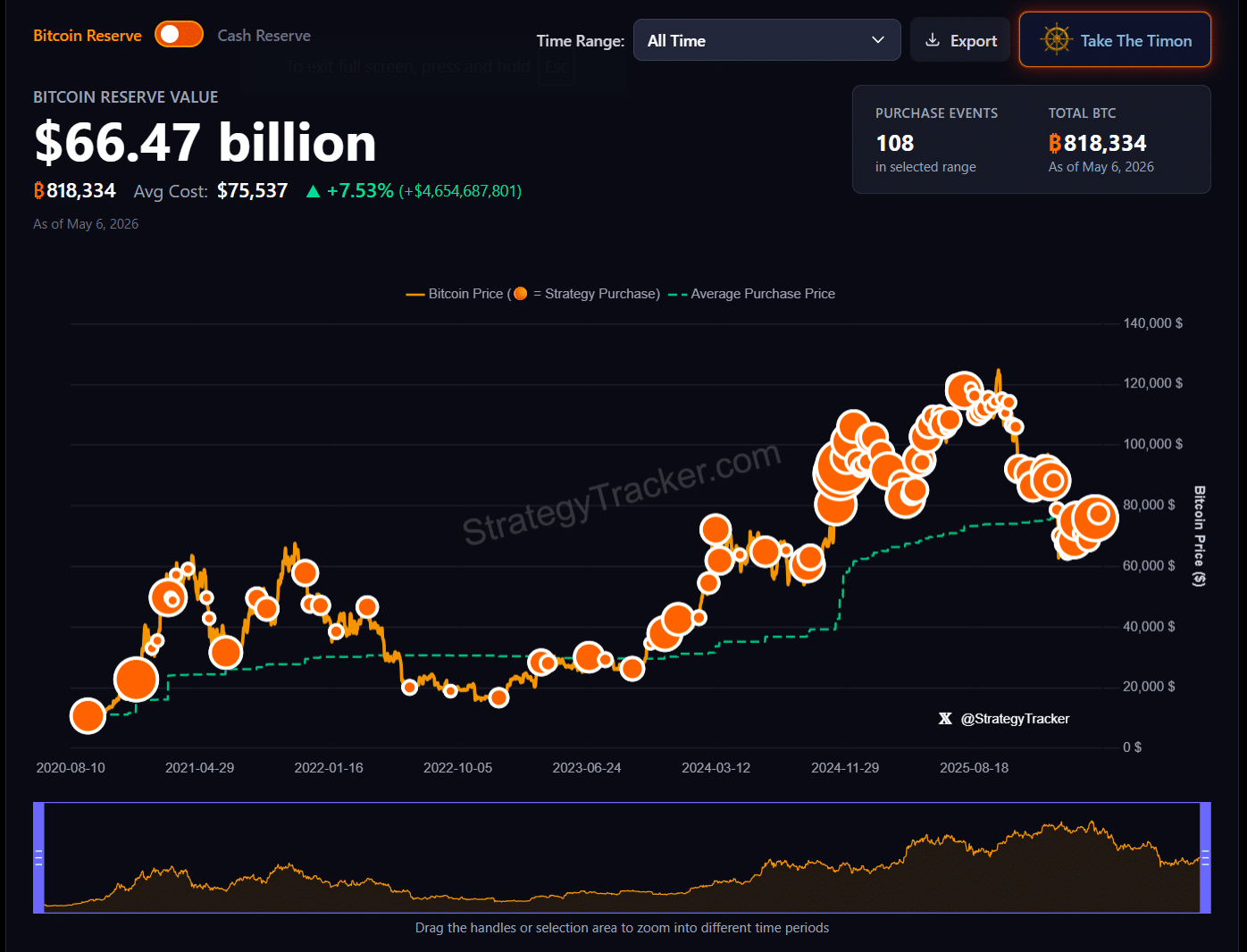

The biggest corporate Bitcoin holder has amassed 818,334 BTC, now worth about $67 billion. With Bitcoin hovering near $81,500, the company is up roughly $4.6 billion on paper.

Explaining the company’s capital framework, Saylor pointed to Bitcoin’s breakeven annual return of about 2.3%. Above this level, Strategy can fund its dividend obligations by selling Bitcoin while still growing its overall Bitcoin holdings, thanks to strong inflows from STRC issuance

In other words, the model is powered by issuing STRC, the company’s preferred stock instrument, and deploying the proceeds into additional Bitcoin. When issuance outpaces the breakeven threshold, new capital raised more than offsets Bitcoin sold for dividends, enabling net Bitcoin accumulation over time.

“We could stop selling MSTR, our common stock right now. We can fund the dividends with Bitcoin sales. And if Stretch issuance is greater than that BTC breakeven number, not only will we fund the dividends forever, we will increase the amount of Bitcoin that we hold forever at the same time,” Saylor said.

“If we were to sell $1.5 billion of Stretch per year, we can sell Bitcoin, pay the dividends, buy more Bitcoin than we sell, grow our Bitcoin stack and generate Bitcoin yield,” he added.

At a 20% annual STRC issuance rate, Saylor projects the company could accumulate an additional 144,000 Bitcoin in a year, even after funding all obligations through Bitcoin sales alone and without tapping equity markets at all.

“You buy Bitcoin with credit, you let it appreciate, and then you sell Bitcoin to pay the dividend,” Saylor said. “As long as you’re issuing credit in excess of the breakeven point, this business works and grows forever.”

In reinforcing the argument, Saylor compared Strategy’s approach to a real estate developer that buys land at $10,000 an acre, sells it at $100,000, and reinvests the proceeds. He argued that this did not undermine the market but reflected rational capital allocation.

“We’re like a Bitcoin development company. We buy it cheap, we sell it dear,” he said. “Capital gains fund credit dividends. That is the essence of the business.”

“And it turns out that sometimes we will sell a Bitcoin derivative because it’s in the best interest of the company, but it’s not necessary,” he added.

The logic, however, rests almost entirely on Bitcoin’s long-term appreciation. Saylor’s conservative model assumes the asset appreciates roughly 10% annually, in line with the historical performance of the S&P 500. His base case assumes 30%.

At either figure, periodic Bitcoin sales are not a concession to market pressure but a deliberate feature of a machine designed to keep accumulating the asset while servicing its obligations, according to Saylor.

Strategy has maintained a strict no-sell Bitcoin policy under its treasury strategy, consistently adding to its holdings via capital markets raises and holding firm through volatility.

Saylor pushed back against “short narratives” suggesting that Bitcoin sales are inherently negative or evidence that Strategy’s model is flawed, but this may not fully eliminate the perception risk in the market.

Strategy’s premium is powered in large part by the long-held belief that the company rarely sells Bitcoin. Even economically rational, well-explained sales may still trigger short-term sentiment pressure.

The company’s shares slipped in after-hours trading, while Bitcoin held steady at above $81,000.

Be the first to comment